History teaches us that even mighty nations fall. A century ago, "The sun never set on the British Empire." Not so today. It would be just as shortsighted for investors to stake everything on their belief that America’s global position will remain dominant. Despite recent advice to the contrary it is still crucial for Americans to invest overseas.

For two decades, the financial planning community touted the "free lunch" benefits of international stocks in U.S. equity portfolios. The theory states that domestic and foreign equity markets provide similar long-term returns but, influenced by various economic factors, will fluctuate in an uncorrelated manner. While the end result will yield at least the same average annual return, the investor’s annual portfolio volatility, or risk, is greatly reduced. The investor who holds non-U.S. stocks will be more comfortable and find it easier to ride out a downturn in the domestic market.

Some advisers, however, have thrown in the towel on international investing. They argue: Expanding capitalism and globalization through decreased trade barriers and increased money flow knocked down more than just the Berlin Wall. International investing no longer reduces risk because as Wall Street goes, so go Tokyo’s Nikkei and Frankfurt’s Dax.

Nonetheless, anyone who has invested in the stock markets of the United States and the rest of the world during the last 25 years can tell you that these markets have not always moved in the same direction. Table 1 compares selected calendar-year returns of an international stock benchmark, the MSCI Europe, Australasia, and Far East (EAFE) index, and a U.S. benchmark, the Standard and Poor’s 500-stock index.

TABLE 1 | ||

| Year | MSCI EAFE | S&P 500 Index |

| 1977 | 18.06 | -7.44 |

| 1982 | -1.86 | 21.46 |

| 1986 | 69.44 | 18.68 |

| 1990 | -23.45 | -3.12 |

| 1992 | -12.17 | 7.62 |

| 1997 | 1.78 | 33.35 |

| 2000 | -14.17 | -9.10 |

Obviously, these selected statistics do not tell the whole story. But first, a brief about the calculation of correlation. The correlation coefficient measures the degree to which the returns of two assets move in step together, based on a scale of —1.0 to 1.0. A correlation of 1.0, or perfect correlation, means that the two assets move together in exactly the same direction. For example, assume asset A increases in value and it is perfectly correlated to asset B. Asset B will also rise over the same period.

The correlation coefficient between the S&P 500 and the MSCI EAFE indices has been rising during the last ten years, meaning that these markets have had more direct relationships. For the ten-year period ended December 31, 2000, the correlation coefficient between the two indices was 0.59. The three- and five-year correlations through December 31, 2000 were 0.78 and 0.73, respectively. Compare this to the long-term correlation of 0.50 since 1970.

Questioning Validity

Some financial planners, after witnessing recent volatility and similar fluctuations between U.S. and foreign markets, argue the benefits of international investing never existed. According to a study by Professors Kirt Butler of Michigan State University and Domingo Castelo Joaquin of Illinois State University, they are partially right. This study illustrates that the diversification benefits of international investing are less than most investment professionals and academics previously thought based on data going back to 1970. The analysis shows that when the world equity markets are experiencing a bear market, the correlations between the largest national equity markets rise. This means that if you are a U.S.-based investor and the U.S. market tumbles, the correlation between it and international markets increases. Therefore you are not receiving the benefits of international diversification right when you need them the most. Much of the downside protection that international investing was previously thought to provide is eliminated. The study concludes that the benefits of international diversification are reduced by as much as 53% as measured by risk-adjusted performance.

Does this mean international investments do not reduce risk? The answer is no. Although the correlations of the world’s largest equity markets are higher in bear markets then previously thought, they are still not perfectly correlated. Whenever you add assets to a portfolio that are less than perfectly correlated, you still gain the benefits of diversification.

There are other international investments that still maintain low correlations to U.S. equity markets. Although they should never represent a major piece of an international stock allocation, international small-company stocks continue to enjoy low correlations to U.S. equity markets.

The T. Rowe Price International Discovery fund, the oldest international small cap fund in Morningstar’s database, has had a very low correlation to the S&P 500 index. For the three- and five-year periods ended December 31, 2000, the correlations were 0.43 and 0.40, respectively. The ten-year correlation coefficient between the fund and the index was 0.39. The correlation is not nearly as great as the one exhibited by the larger stocks.

World of Opportunities

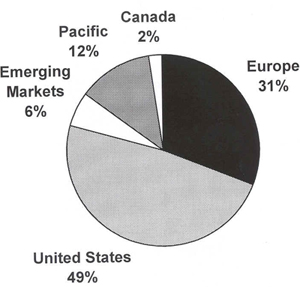

With over 50% of the world’s equity market capitalization existing outside of the United States, investors who choose to limit their investments to U.S. companies will be missing out on many opportunities.

| World Equity Market Capitalization (January 31, 2001) Source: Morgan Stanley Capital International |

|

Thousands of well-run companies are domiciled outside of the United States. Consider the products common in our culture whose parent companies are based outside our borders. Sales of Sony DVD players, Heineken beer, and the 2001 Motor Trend Car of the Year, (Daimler) Chrylser’s PT Cruiser, all reach the bottom line of non-U.S.

companies.

Additionally, there are industries and products where U.S. companies do not have the upper hand. For instance, there are non-U.S. companies that are much further advanced in the

development of alternative sources of energy.

While it’s good to be the King, the U.S. may not always be the star of the global show. Our economy may cool while other regions that adopt strongeconomic policies enjoy sustainable growth. Assuming the European Monetary Union experiment succeeds, its economic expansion has the potential to rival the one we have experienced. And China, despite its political system, will be a fierce market competitor during this century. Complacency is a disease that must be avoided. At Palisades Hudson Asset Management, Inc. we continue to recommend a 25% overseas allocation for our U.S.-based clients’ equity portfolios. While many U.S. companies provide goods and services throughout the globe, the relationship is not a one-way street.

Years ago, when I was studying international business in London, an American student consuming a Kit-Kat candy bar complained about the looks of the British wrapper—it was "wrong." She pondered out loud when Europeans started enjoying this brilliant American invention. The professor, brimming with pride, informed the class that Kit-Kat was developed in the U.K. and "exported to the colonies."

If Americans choose not to invest overseas, we are gambling that our position and advantages will exist forever. History has told us they will not.