Congress met President Donald Trump’s deadline by passing a budget reconciliation bill in time for him to sign it into law July 4, 2025. Now that the “big beautiful bill” is law, it is time for taxpayers and tax professionals to unpack its effects.

The One Big Beautiful Bill Act, often shortened as OBBBA, is a major piece of legislation with a final text hundreds of pages long. I will not be able to cover even the tax effects comprehensively in this article. While I plan to discuss the major changes relevant to personal income tax, every taxpayer’s situation is unique. If you don’t work with a tax professional every year, consider checking in with an expert as you prepare your documents for tax year 2025. This advice applies doubly to taxpayers with international tax concerns or who are business owners.

What’s Staying The Same?

A major component of the OBBBA was making permanent a variety of tax changes initially created by the Tax Cuts and Jobs Act in 2017. Many of that law’s provisions were set to end after 2025 but have now been preserved with no built-in end date.

Income Tax Rates And Brackets

One of the most fundamental examples of provisions the OBBBA made permanent: individual income tax rates and tax brackets. The new law locks in changes from 2017 that otherwise would have reverted after this year. And while the TCJA didn’t change tax rates for long-term capital gains, it did modify the brackets, and those changes are now permanent as well. Similarly, the OBBBA locked in the standard deduction’s higher rate and updated indexing formulation going forward. It also slightly boosted the standard deduction for 2025, which is now $15,750 for single filers and $31,500 for married taxpayers filing jointly.

Alternative Minimum Tax

The new tax package locks in changes to the alternative minimum tax, or AMT. The 2017 tax package increased exemption amounts, which meant AMT applied to fewer taxpayers. This will now remain the case indefinitely. The OBBBA did, however, revert the exemption phaseout thresholds for AMT to their 2018 levels, indexed for inflation going forward. The new law also increased the phaseout exemption amount. Instead of 25% of the amount by which the taxpayer’s “alternative minimum taxable income” exceeds the threshold, the exemption amount is now 50%. In addition, the OBBBA changed the cap on state and local tax deductions (which I will discuss in more detail later in this article). These deductions can affect whether taxpayers are subject to AMT rules, so taxpayers in high-tax states should take special care in determining whether their situations have changed. AMT can be complicated, so taxpayers who think it might apply should still consult a tax professional.

Qualified Business Income

One of the Tax Cuts and Jobs Act’s major changes to existing taxation was the creation of a deduction for qualified business income, or QBI. Since this article isn’t meant to focus deeply on business taxes, I won’t get into the full details of how QBI deductions work. However, the OBBBA did make this deduction a permanent feature of our federal taxation architecture, and QBI is an eligible deduction for individuals in the same manner as it was under the TCJA. The new law made some slight adjustments to phaseout rules, but otherwise preserved the QBI deduction much as it has existed for the past seven years.

Mortgage Interest Deduction

In the TCJA, Congress limited the qualified residence mortgage interest deduction to the first $750,000 of mortgage debt (with exceptions for certain older mortgages). The new law makes this limitation permanent. It also permanently excludes interest on home-equity debt from the mortgage interest deduction, unless those funds are used to buy, build or substantially improve a primary residence. Homeowners who have gotten used to this change can count on it sticking around unless a future Congress proactively changes it.

What’s Changing A Little?

In addition to extending changes that formerly came with an end date, the OBBBA made a few changes that did not qualitatively modify the existing rules but did adjust the limits, thresholds and other dollar amounts involved. Some of these changes could have significant effects for particular taxpayers.

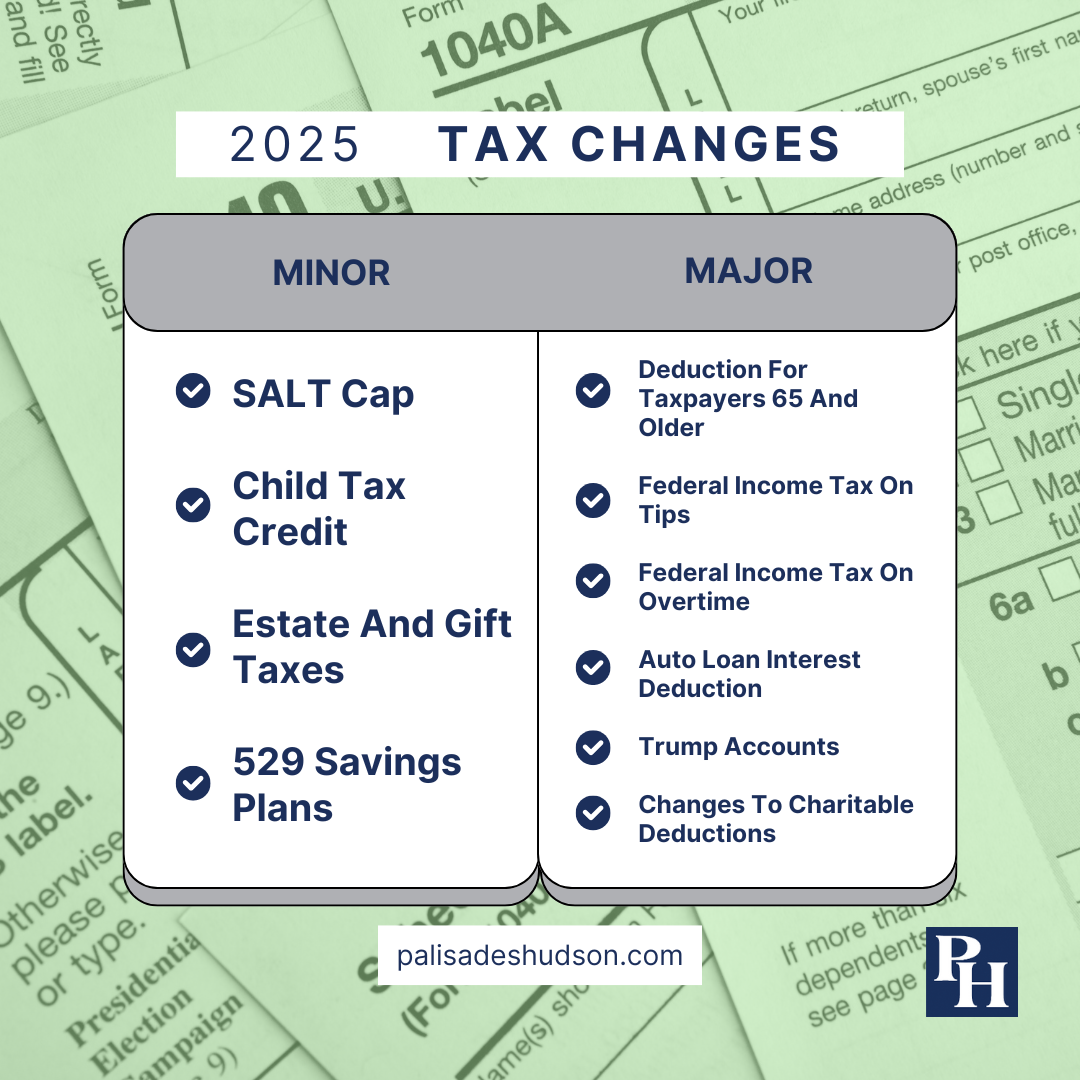

SALT Cap

One large tax change that Congress introduced in 2017 was to limit federal income tax deductions for state and local taxes. The SALT deduction was capped at $10,000 per taxpayer per year. This change was especially significant for taxpayers in high-tax states, where the annual sum of state income taxes and property taxes may greatly exceed the $10,000 cap.

The OBBBA raised this cap to $40,000 for tax year 2025, with a 1% increase annually in each of the four years that follow. This cap phases down for taxpayers with modified adjusted gross income at or above $500,000, leveling out at $10,000. This income threshold will also increase by 1% each year. The SALT cap reverts to $10,000 for everyone in 2029, unless Congress acts to modify or raise it before then.

The Child Tax Credit

The Child Tax Credit is not significantly changing, but the OBBBA did raise the amount to $2,200 per child, up from $2,000. This amount will be indexed for inflation going forward. The $200 increase goes to the nonrefundable part of the tax credit, which means it only helps taxpayers who already owe enough tax to qualify for the full amount.

Additionally, the Child Tax Credit joins several other provisions of the tax code that specify that a taxpayer — or, in the case of this credit, his or her spouse — must have a Social Security number to qualify. Formerly, taxpayers could claim this credit as long as the children had Social Security numbers, regardless of whether the parents had their own.

Estate And Gift Taxes

The TCJA raised the lifetime exemption for gift and estate tax, and the OBBBA not only preserved that increase but raised the amount further. The new exemption is $15 million per individual in 2026, indexed for inflation going forward. This new exemption threshold will also apply to the lifetime exemption for generation-skipping transfer tax. This change means that even fewer families will need to worry about federal estate and gift taxes, at least for the time being. (For more on estate tax and GST tax basics, check out the podcast episode “Why Estate Planning Is For Everyone,” featuring my colleague David Walters.)

529 Savings Plans

The 2017 legislation package expanded the definition of qualified educational expenses for Section 529 savings plans to include up to $10,000 per year for elementary or secondary school tuition. The new legislation expands this change in two ways. First, it broadens qualified expenses again to include books, supplies, tutoring, and a variety of other related educational costs for K-12 students. It also raises the annual limit for primary and secondary expenses to $20,000 per year.

In addition, the new law broadens the list of qualified expenses related to workforce, on-the-job and continuing education training. Contribution rules and rules governing nonqualified withdrawals remain the same.

What’s Changing Significantly?

Congress made changes above and beyond simply preserving or expanding provisions of the TCJA. Many of these new changes, while not permanent, are the fulfillment of (or are at least related to) Trump’s campaign trail promises.

New Deduction For Older Adults

Despite some confusion the Social Security Administration caused in early July, the OBBBA does not make any direct change to how the government taxes Social Security benefits. Instead, taxpayers age 65 or older can now deduct an additional $6,000 from their income. This deduction phases out at a 6% rate for individual filers with modified adjusted gross income above $75,000 ($150,000 for married couples filing jointly, if both spouses are over 65). The deduction disappears completely at a MAGI of $175,000 for individuals or $250,000 for joint filers. This deduction is available regardless of whether a taxpayer itemizes or takes the standard deduction. It also stacks with the existing standard deduction tax break for those over 65 (an extra $2,000 per taxpayer, or $3,200 for couples filing jointly).

This new deduction could, for some taxpayers, indirectly impact how much of their Social Security income is subject to tax. However, lawmakers could not make direct changes to Social Security benefit taxation as part of a reconciliation bill, so the deduction for older taxpayers is an indirect approach to achieve this goal. Like the Child Tax Credit, this new deduction requires taxpayers to have a Social Security number in order to claim it. Unless lawmakers extend it, the deduction will sunset after tax year 2028.

No Tax On Tips

For tax years 2025 through 2028, taxpayers who earn tips will (with some exceptions that I will discuss) be able to deduct up to $25,000 of tips from their taxable income. Note that, even for taxpayers fully eligible for this deduction, this change will not exempt tip income from state income taxes or payroll taxes, so it does not make tips fully tax-free. Tips still also contribute to adjusted gross income, but the deduction is available even to taxpayers who do not itemize deductions.

The deduction on tips phases out once a taxpayer’s modified adjusted gross income exceeds $150,000 ($300,000 for joint filers). After this threshold, the deduction decreases by $100 for each $1,000 by which MAGI exceeds this amount. Self-employed taxpayers who earn tips cannot deduct an amount greater than their business’s gross income for the year.

To be considered a “qualified tip” for the purposes of this deduction, the income must come from a person paying it voluntarily, with no consequence if they decline to pay. This would, for example, disqualify mandatory service charges or resort fees. The tip cannot be subject to negotiation, and it must be currency rather than tangible items, tickets, passes or other assets. The law also specifies that taxpayers who deduct tips must hold jobs that traditionally elicit tips; the Treasury Department will publish a list of the occupations that meet this requirement no later than early October 2025.

No Tax On Overtime

In a similar approach to the tip deduction, the OBBBA exempts overtime income from federal income tax through tax year 2028, within certain limits. Taxpayers making $150,000 or less ($300,000 for joint filers) can deduct up to $12,500 ($25,000) in overtime income. Also like the deduction for tips, the overtime deduction phases out by $100 for each $1,000 of income over the threshold. The overtime deduction is available to taxpayers who take the standard deduction as well as those who itemize.

Taxpayers should stay mindful that, again like the deduction for tips, any deducted overtime income is still subject to payroll and state income taxes. Taxpayers should note, too, that a given dollar of income can only go toward the tips deduction or the overtime deduction, not both.

While Form W-2 already breaks out tips, many employers will need to make changes to how they track their employees’ earnings in order to reflect this new deduction’s provisions. Congress stipulated that employers may use a “reasonable method,” as outlined by the Treasury Department, to approximate this income for 2025, since businesses are already more than halfway through the calendar year. The deduction will only apply to overtime required by the Fair Labor Standards Act, and so will not apply to overtime stipulated only by contract, collective bargaining or state law. Given the complications of tracking overtime income, taxpayers should take extra care with this deduction, especially for tax year 2025.

Auto Loan Interest Deduction

Starting in tax year 2025, taxpayers will be able to take a deduction of up to $10,000 for loans used to purchase automotive vehicles as long as the purchased vehicle was assembled in the United States. This is yet another deduction that is available even to taxpayers who do not itemize their deductions.

The auto loan interest deduction phases out with income above $100,000 ($200,000 for couples filing jointly). For each $1,000 above the threshold, the deduction decreases by $200. Like the other deductions I’ve discussed in this section, this new deduction will expire after tax year 2028 unless lawmakers act to extend it.

Taxpayers purchasing vehicles should also note that the existing tax credit for buying an electric vehicle will now expire on Sept. 30, 2025.

Trump Accounts

These new accounts — called the Money Accounts for Growth and Advancement accounts in a draft version, but simplified to “Trump accounts” in the final text of the law — let parents save for their child’s future educational, entrepreneurial or housing needs. Parents or guardians of children 8 years old or younger may contribute up to $5,000 per year. Distributions will be taxed at ordinary income tax rates when beneficiaries age 18 or older use account assets to fund higher education, start a business or purchase a first home.

The OBBBA also calls for a one-time government contribution of $1,000 to these accounts for children born between Jan. 1, 2025 and Jan. 1, 2029. To be eligible, children must be U.S. citizens at birth and at least one parent must have a Social Security number.

Charitable Contributions

Since the current high standard deduction means fewer taxpayers find it worthwhile to itemize deductions, many taxpayers who once deducted charitable contributions no longer do so. The OBBBA creates an “above the line” deduction — available to taxpayers who do not itemize their deductions — for contributions up to $1,000 ($2,000 for joint filers). These charitable contributions must be cash, not appreciated assets, and they must go directly to an eligible nonprofit organization. Contributions to private foundations or donor advised funds are not eligible, for example.

For taxpayers who do itemize, the OBBBA established a new floor on itemized charitable deductions. Effective for tax years after 2025, taxpayers must now meet a minimum threshold of charitable contributions equal to 0.5% of their income in order to deduct them. For example, a taxpayer who makes $150,000 a year would only benefit on contributions over $750. The new law also makes permanent the existing cap of 60% of adjusted gross income on cash gifts to qualified charities.

The OBBBA is a sweeping piece of legislation, and while I have tried to cover the most significant individual income tax changes for the largest number of taxpayers, you may find other changes relevant to you among the law’s many provisions. Given that many of the changes in the law take effect for tax year 2025, it is worth reaching out to your tax professional well in advance of the end of the year. This will give you plenty of time to make any changes in your tax planning that you wish to pursue.

As my colleagues and I have written in the past, no tax law is ever truly permanent. But with this new legislation, taxpayers and tax planners alike can see the shape of the next several tax years a bit more clearly.