Some drivers are drawn to electric cars because of reduced environmental impact, while others appreciate the lower lifetime fuel costs and reduced maintenance. Another potential bonus is money back in your pocket from tax incentives — if you can navigate the process.

Legislators offer a variety of tax benefits to taxpayers who purchase electric vehicles. But determining which incentives apply can be confusing. If you’re interested in going electric, or if you’ve gone electric recently and wonder how it might affect your taxes, we will walk you through the basics. First, though, it may be helpful to put electric vehicles in context.

A (Not So) Brief History of EVs

Incredible as it seems, electric vehicles made up one-third of automobiles on the road in a major U.S. city in the year 1900. At the time, New York City had a fleet of 60 electric taxis, and many customers preferred the quiet, odorless ride that they couldn’t get from gasoline and steam vehicles. After Ford released the Model T in 1908 and assembly line production became standardized, manufacturing costs of gasoline-powered vehicles dropped quickly. Electric vehicles were soon priced out of the market.

Fast forward through two world wars and an oil crisis. By the 1960s and 70s, electric vehicles were once again piquing interest in the auto industry. The combination of rising gas prices and the early stages of climate change research in this era reignited a demand for vehicles fueled by sources other than gasoline. That demand has not died down since. Believe it or not, it’s been over 25 years since Toyota released the well-known (and mostly loved) Prius hybrid to global markets. Today, both hybrid and fully electric vehicles are mainstream options.

While EVs are not yet a dominant force in auto sales, they are making up ground rapidly (notwithstanding a recent sales slowdown). In 2022, consumers purchased 918,500 new light electric vehicles, more than double the number sold in 2018 despite production bottlenecks constraining availability. As of the third quarter of 2023, sales were projected to surpass 1 million for the year. Analysts at Morningstar predict that, by 2030, EVs will account for roughly 40% of auto sales worldwide.

Even with millions of EVs and hybrids already on the road and more on the way, buyers may not be familiar with potential tax benefits they can gain by purchasing or leasing new or used electric vehicles. Yet while the specifics have changed, the broad fact of U.S. government support for EVs is nothing new, either. Legislators began incentivizing research into hybrids and EVs in the 1990s through various pieces of climate and energy legislation. The government continues to support the EV industry today, including through consumer incentives. As a result of the 2022 Inflation Reduction Act, buyers can directly benefit from tax credits when purchasing a qualifying EV.

As with many parts of the tax code, however, the rules for claiming EV tax credits are far from simple. The following breakdown will help you to navigate the process of claiming the current available credits and help you to know what to look for if you are in the market for an EV.

Navigating EV Tax Credits

A few standard rules apply to all of the tax credits we will discuss. First, all EV-related tax credits are nonrefundable. This means that if the credit exceeds a filer’s tax liability, the filer will not receive the difference as a refund. In other words, you can only receive credit up to the tax you would otherwise owe. Also, filers cannot apply the credit to future tax years.

Second, to satisfy income requirements, filers can use their modified adjusted gross income, or MAGI, from the year they take delivery of the vehicle or the year before — whichever is less. If the taxpayer’s MAGI is below the threshold in either of the two years, he or she can claim the credit. Vehicles must be purchased for personal use (or business use, if claiming the commercial clean vehicle credit, which we will discuss later in this article). The Internal Revenue Service also requires buyers to use the vehicle mostly in the U.S.

Finally, note that there are no upper limits on the number of credits per household or business, but filers must submit separate forms for each vehicle purchase in order to claim multiple credits.

New EVs Purchased In 2022 Or Earlier

If taxpayers purchased their EVs in 2022 or earlier, they must file an amended return for the year in which they took possession of the vehicle if they wish to retroactively claim the credit. This means that buyers who purchased vehicles prior to 2018 are out of luck, as amended returns cannot be submitted more than three years following the original tax return’s due date (or, in atypical circumstances when the tax was paid later, within two years after the tax was paid).

Vehicles purchased in 2022 or earlier are only eligible for the full credit if their manufacturer has sold less than 200,000 EVs in the United States. Buyers can check the status of each EV manufacturer on the IRS website. For the two quarters after the company reached the sales quota, buyers could still receive 50% of the credit. In the third and fourth quarters after the milestone, the amount decreased to 25%. After a year, all vehicles from the manufacturer were no longer eligible for the credit. Tesla, the best-known EV maker in the United States, passed this benchmark in 2018, and thus the credit phased out for Teslas purchased between 2020 and 2022. (Note, however, that the rules for EVs purchased in 2023 changed again, as we will discuss in the next section.)

Additionally, to be eligible for the credit, the vehicle must use an external charging source and have a gross vehicle weight rating of less than 14,000 pounds. For vehicles bought after Aug. 16, 2022, final assembly must have occurred in North America. The Department of Energy has created an online database to assist consumers in checking the assembly history of different EV models. If the vehicle purchase took place before Aug. 16, 2022 but the buyer received the car after that date, taxpayers can elect to claim the credit based on the earlier rules.

If the vehicle qualifies based on the criteria above and the taxpayer can still file an amended return, buyers can receive a credit of $2,917 for a vehicle with a battery capacity of at least five kilowatt hours (kWh), plus $417 for each kWh of capacity over five kWh, up to a maximum credit of $7,500. To claim, taxpayers can file an amended return for the year they took possession of the vehicle. The amended return should include a completed Form 8936.

New EVs Purchased In 2023 Or After

If a taxpayer purchased a new EV in 2023 (or later, assuming the current rules remain in place), the taxpayer does not need to consider the number of cars the vehicle’s manufacturer previously sold when determining eligibility for tax credits. However, income restrictions apply. To claim the credit, a filer’s modified adjusted gross income cannot be more than:

- $300,000 for married couples filing jointly

- $225,000 for heads of households

- $150,000 for all other filers

To qualify for this credit, vehicles must be bought brand-new and final assembly must occur in North America. As with other EV credits we have discussed, credit for a new EV purchased in 2023 or later is contingent on the vehicle having a battery capacity of at least seven kilowatt hours and a gross vehicle weight rating of less than 14,000 pounds. The EV’s manufacturer suggested retail price must also be less than $80,000 (for vans, sport utility vehicles, and pickup trucks) or $55,000 (for all other vehicles).

EVs are subject to different tax credit requirements and earn different credit amounts depending on whether they went into service before or after April 17, 2023. If a vehicle went into service between Jan. 1 and April 16 and meets all of the criteria we mentioned in the previous paragraph, the buyer qualifies for a minimum credit of $3,751, plus $417 for each additional kilowatt hour of battery capacity beyond seven, up to a maximum credit of $7,500. Vehicles placed in service on or after April 17, 2023 must also meet the IRS’s new critical mineral and battery component requirements to qualify for any credit, even if the taxpayer purchased the EV before that date. If a vehicle meets both the battery and critical mineral requirements, it qualifies the purchaser for a credit of $7,500. If the vehicle only meets one of the two requirements, the purchaser qualifies for a credit of $3,750. If a vehicle does not meet either requirement, it is not eligible for any credit.

Regardless of when taxpayers bought their vehicles or put them into service, taxpayers seeking a tax credit for a new EV should be aware that the seller must provide the IRS with certain information at the time of sale. This includes the buyer’s name and taxpayer identification number (in most cases, this is your Social Security number). Recently, the IRS created an online tool for dealers to register their businesses and submit time-of-sale reports. Beginning in 2024, sellers will submit all relevant information through this tool.

When purchasing a qualifying EV, buyers should make sure they encourage and trust the seller to fulfill their side of responsibilities; otherwise, they risk missing out on the tax credit from the purchase. Additionally, the seller must directly provide the buyer with documentation of information including the vehicle’s identification number, battery capacity, sales price, and confirmation that the buyer is the original user if the vehicle is new. The buyer will need this data to complete Form 8936. The taxpayer should submit this form in the year he or she purchased an EV.

Used EVs

As of Jan. 1, 2023, the purchase of pre-owned EVs can also qualify taxpayers for a credit. The tax credit available for purchasing a used EV involves different rules than purchasing a new EV. First, it carries the following income limits:

- $150,000 for married filing jointly or a surviving spouse

- $112,500 for heads of households

- $75,000 for all other filers

To qualify, the buyer must have purchased the pre-owned vehicle from a registered dealer for no more than $25,000. This maximum sales price includes all dealer-imposed costs and fees, but not costs required by law, such as taxes or title and registration fees. As with the purchase of a new EV, the seller must report certain information to the purchaser and to the IRS in order for the buyer to receive the credit.

Additionally, the model of the vehicle must be at least two years old at the time of purchase. For example, if you buy a vehicle in 2023, it would need a model year of 2021 or older to qualify for the credit. The EV must have a gross vehicle weight rating of less than 14,000 pounds and a battery capacity of at least seven kilowatt hours. The vehicle also cannot be on its second resale; the transaction must represent its first resale since Aug. 17, 2023. The Department of Energy has created a useful online resource to check which makes and models qualify for the federal tax credit for plug-in electric and fuel cell vehicles. This index, along with the IRS’s Used Clean Vehicle Tax Credit Checklist, will likely come in handy for taxpayers who want to know whether the credit will apply to their planned vehicle purchase.

If your vehicle satisfies all of the above requirements, you can claim the used EV tax credit by completing Form 8936 with your tax return in the year you took possession of the vehicle. Businesses cannot claim this credit, and any vehicles purchased before 2023 are not eligible. The value of the credit equals 30% of the sale price, up to a maximum of $4,000.

Leasing EVs

Taxpayers may not need to purchase an EV to benefit from the clean vehicle credits that Congress established in the Inflation Reduction Act. Consumers interested in leasing could experience indirect savings, but only if the lessor is willing to pass along the credit that they receive. According to Consumer Reports, many automakers are indeed choosing to pass on savings to buyers “through an advertised discount.” By subtracting the full or partial credit amount from the overall vehicle price at the time of signing, lessees save by incurring lower monthly payments. However, because this choice remains with the lessor, it is important to pay attention to detailed pricing breakdowns. Ask questions if a lessor’s descriptions of potential discounts are vague or are not itemized. This way you can understand upfront whether the clean vehicle credit is affecting your lease.

The Commercial Clean Vehicle Credit

Businesses and tax-exempt organizations seeking to claim a clean vehicle tax credit are subject to a separate set of rules. To qualify, the entity must purchase the vehicle from a qualified manufacturer, and the EV cannot be eligible for the individual clean vehicle tax credit. (In other words, the IRS does not allow a “double dip” in which an individual and a business both claim the credit for the same purchase.) The motor must be a fuel cell or have a battery capacity of at least seven kilowatt hours if it weighs less than 14,000 pounds, and 15 kilowatt hours if it weighs more. The credit is equal to the lesser of 15% of the buyer’s basis in the vehicle (30% if the vehicle uses no gasoline or diesel) or the incremental cost of the vehicle. The maximum credit limit is $7,500 for vehicles with a gross vehicle weight rating less than 14,000 pounds, and $40,000 for all other vehicles. The IRS is still working on a form for eligible filers to claim this credit, so stay tuned. Maintaining organized purchase and vehicle records will help you complete the form once it becomes available.

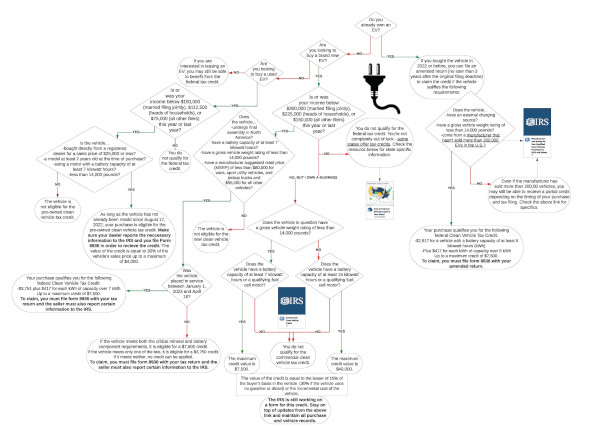

As you can see, many factors can affect whether you qualify for federal EV credits and what amounts you can receive. We have created a flow chart to help you visualize some of these variables. Click below to enlarge.

State Credits And Penalties

Certain states have enacted their own tax policies to incentivize residents to choose EVs. Other states have created penalties designed to offset potential lost revenue from the state’s gasoline tax. Contradictory as it is, some states have both.

The details of the penalties vary by state. Some (like Hawaii, West Virginia and Ohio) charge increased vehicle registration fees for EVs. Others (including Georgia, Oklahoma and Utah) tax the electric output from EV charging stations. Although some of these policies are already in effect at this writing, many are slated to take effect in the next three to five years as policymakers prepare for continuing changes to the composition of vehicles on the roads.

Don’t assume your state’s policy will look a certain way based on the prevailing political climate. California, for example, offers a tax credit with a value ranging from $750 to $7,500 for qualifying EVs, but it charges an additional fee of about $100 to register EVs with the state’s DMV. Kansas offers an EV tax credit of up to $2,400, but charges slightly higher registration rates for both EV and hybrid vehicles. If you are considering an EV purchase, it is important to stay up to date with your state’s rules to ensure you understand the true cost of your purchase based on your location.

The eligibility requirements and credit amounts for EV tax credits, at both the state and the federal level, will likely continue to change as more automakers release fully electric vehicles and the number of EVs on the roads continues to rise. For instance, the IRS recently announced that, beginning in 2024, taxpayers will be able to transfer the credit to the dealership in order to experience upfront savings on the cost of the vehicle, rather than waiting for a reduced tax liability when filing that year’s return. IRS publications or third-party summaries of these publications are great resources to stay up to date on future policy changes. As always, an experienced tax adviser will be able to provide customized guidance on your personal situation.

EV tax credits offer opportunities for substantial savings. Taxpayers shouldn’t overlook these potential benefits just because the specifics are complicated. Taking the time to understand the rules, at both the federal and state level, can help you make the most of your purchase.