If you keep an eye on the news, you know that U.S. interest rates are higher than they have been in nearly 20 years. You may be less sure on what this means for your personal financial picture.

The Federal Reserve has raised the federal funds rate — the interest rate at which banks lend to and borrow from one another overnight — 11 times since March 2022. This represents the fastest rate of increase since the early 1980s. At this writing, the target federal funds rate is between 5.25% and 5.5%, the highest level since 2007.

The Fed kept the rate low for nearly 14 years following the Great Recession, trying to encourage a sluggish economic recovery. More recently, the central bank opted to cut interest rates because of the COVID-19 pandemic and its potential negative effects on the economy. But as inflation spiked in 2022, the Fed changed its approach. Raising the federal funds rate was an attempt to pull inflation back down to the central bank’s target of 2%. As I write this article, inflation remains just above 3%, which is over that target but a distinct improvement from inflation greater than 9% in June 2022.

I’ve said that the Fed adjusts the federal funds rate, but you may often hear it said that the Fed is raising or lowering “interest rates” more broadly. This is because, while the federal funds rate is not something that consumers pay directly, the rate usually triggers a domino effect on other market interest rates. When banks pay more to borrow, they typically pass that cost on via the interest rates they offer consumers on products including personal loans, business loans, mortgages and credit cards. They may also try to entice savers by offering higher rates on certificates of deposit, money market accounts or other savings vehicles. Expectations about the future of the federal funds rate can also affect Treasury yields, which in turn affect the prices of many other forms of business or government-backed credit, as well as mortgages and other consumer debt.

If you are under 50, interest rates have been declining or near zero for much of your adult life. The rapid increases of the past two years may therefore seem daunting. While interest rates remain well below the highs of the 1980s, when mortgage rates approached 20%, they have arrived following a historically unusual stretch of remaining near zero. Many people may be anchored to low interest rates; others may just be wary of the unknown.

That said, like many economic phenomena, higher interest rates are neither purely beneficial nor purely challenging. Adjusting your mindset can help you to make the most of higher rates where they benefit you and cushion the impact where they may otherwise hurt.

Higher Interest Rates For Borrowers

The first major adjustment when moving from a low interest rate environment to a higher interest rate environment is internalizing the idea that borrowing is no longer “free.” When interest rates hovered near zero, consumer loans and credit cards carried corresponding low interest rates. This gave borrowers substantial flexibility and, in some cases, allowed them to live beyond their means.

While living beyond your means is never ideal, the costs are substantially higher now than they were a few years ago. Credit cards’ average interest rate recently hit an all-time high of 21%. Compare these rates with an average credit card interest rate of 16.34% in March 2022. Retail credit cards — those associated with a particular store or vendor — have reached an average rate of 28.93%. Since most credit cards carry a variable interest rate, cardholders generally will not have been able to lock in lower rates from the time they opened their accounts. Credit card debt is high-cost in any interest rate environment, but even so, it is especially pricey right now.

The results are becoming obvious: A report from WalletHub in late 2023 projected that U.S. consumers would end the year with $100 billion more credit card debt than they carried the prior January. The Federal Reserve Bank of New York’s Center for Microeconomic Data reported in November that American credit card debt had reached a collective $1.079 trillion.

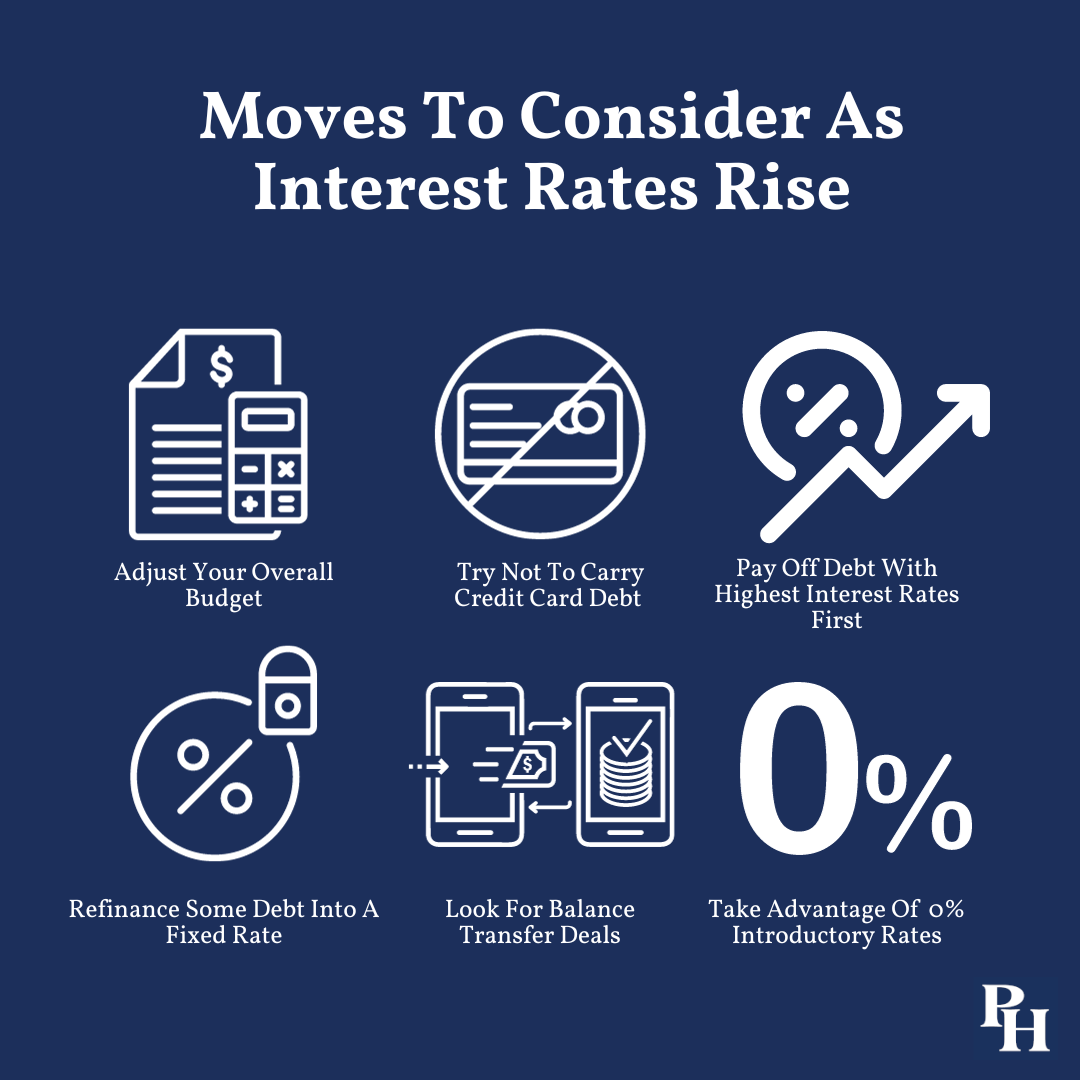

If you don’t currently carry credit card debt from month to month, do your best to keep up this positive habit. And if you do currently carry a balance, consider forming a plan to pay it down as soon as you practically can.

Servicing your credit card debt, or any variable debt, can become increasingly difficult as interest rates rise. When you make a plan, consider focusing on the debt with the highest interest rates first, paying special attention to debt that could become more expensive if rates go up more. If possible, you may want to consider refinancing some of your debt into a fixed rate. You may also want to look for balance transfer deals or 0% interest introductory rates, but you should aim to pay off the debt before the introductory period ends. If you can’t, you should make sure the interest rate after the introductory period is manageable and won’t derail your debt repayment plan.

You may also need to readjust your overall budget to reflect the new economic reality. Federal student loan rates are fixed, so existing borrowers’ rates will not increase. But new undergraduate borrowers will pay up to 5.5% on federal student loans for the 2023-24 academic year. Graduate and professional degree borrowers will pay a rate of 7.05%. In addition, many borrowers haven’t had to pay their student loans over the last several years, and the accrual of interest on their loans was paused. Resuming payments (and accruing interest again) may have unwelcome effects on borrowers’ budgets. Government borrowers may want to investigate the available repayment plans, including the Saving on a Valuable Education (SAVE) option introduced in 2023, if they are having trouble keeping up with payments. Private student loans are more likely to carry variable interest rates, though the degree of change will depend on the benchmark the loan uses. Borrowers should keep an eye on their interest and focus on paying off high-interest loans first when possible.

Existing auto loans generally carry fixed interest rates, but if you need a new car, expect to pay more too. Car prices and the interest rates on new auto loans have both risen. Bankrate reports that the average rate on a five-year new car loan recently was 7.72%. While car affordability has shown signs of improvement, it may be a good time to try to get as much life as you can out of an older car, especially since ongoing constraint on supply means buying a used vehicle is not the source of savings it once was.

Overall, when it costs more to borrow, borrowers are rewarded for comparison shopping to the extent they are able. When interest rates were low, the difference between rates for personal, auto or business loans may have been relatively minor. Borrowers should remember that shopping around for rates is especially important now that those rates are higher.

Higher Interest Rates And The Housing Market

While the housing market is a subset of borrowing, interest rates can have an especially large effect on individuals and families when it comes to mortgages.

Many people who purchased homes or refinanced existing mortgages in the span between 2008 and 2022 secured mortgage rates well below historical averages. While there are certainly upsides to this scenario, these mortgages can also serve as “golden handcuffs,” keeping homeowners where they are when they might otherwise move on. People are understandably reluctant to sell a home with a mortgage that’s less than 4% at a time when 30-year mortgage rates may top 7%. This reality causes a ripple effect for new buyers, or buyers for whom moving is not optional. Homeowners staying put has constricted the supply of existing homes available for sale. This, in turn, has kept home prices elevated, especially in desirable locations. Potential buyers are hit with the one-two punch of higher mortgage rates and high home prices. This means buyers have generally lost significant purchasing power. As far as it is within your control, you may want to delay homebuying until the market is more favorable.

Homeowners who are reluctant to let their pre-2022 mortgage rate go might want to consider renovating their current home. The high prices that contribute to keeping homeowners in place also mean that many of those homeowners have a significant amount of equity tied up in their homes. Tapping that equity can be a smart way to upgrade their properties. Either a home equity loan or a home equity line of credit, often abbreviated HELOC, can let homeowners make the most of their equity while staying in place. However, defaulting on a home equity loan or HELOC can have serious consequences, including losing a home, so those pursuing this strategy should proceed with care.

Of course, not all homebuyers have the option of delaying their search. If you are looking to buy and can’t wait for a more favorable market, be wary of the concept “marry the house and date the rate.” Don’t purchase a home that you can’t realistically afford over the long term at its current interest rate with the idea of refinancing when rates fall. No one can be sure when rates will go down again, or by how much. If rates don’t descend as quickly as you anticipate, you could do serious harm to your finances. Similarly, while adjustable-rate mortgages can have upsides, they should not be a license to buy more house than you can actually afford on the theory that rates may fall in the future.

Higher Interest Rates For Savers

Rising interest rates mean borrowing isn’t free, but they also mean that, for the first time in a long while, it may pay to be a saver.

Savers had few options for earning a decent return on their money while interest rates were unusually low. That is beginning to change. The Federal Deposit Insurance Corporation has reported that savings account rates at large retail banks have inched up to nearly 0.5% — still not much to shout about, but a notable change after years of practically nothing. Still, savers can likely do better.

Annual percentage yields on high-yield online savings accounts now exceed 5% in some cases, up from around 1% in 2022. Moving from a regular savings account to a high-yield savings account can help you to take advantage of the current interest rate environment. Like regular savings accounts, high-yield savings accounts are federally insured, so they are suitable for emergency funds and other assets you want to keep somewhere stable. You may also want to consider options including money market accounts (though be aware of monthly fees’ potential to eat into your gains) or certificates of deposit (which often offer even higher returns, but require you to leave your deposits untouched for a longer period of time.) Which of these is right for you will depend on your situation, but they are worth considering.

Savers looking for safe places for short-term savings may also want to consider short-term Treasury bills. These instruments mature in periods ranging from four weeks to 52 weeks. At this writing, three-month Treasury bills earn more than 5%, making them more attractive than traditional savings accounts and competitive with high-yield savings accounts. Interest on Treasuries has the added benefit of being exempt from state taxation. For those who pay state income taxes, the after-tax return on your earnings on Treasuries can be higher than what you would get on a CD or a high-yield savings account, even if the rates are similar.

Higher Interest Rates For Investors

Investors should generally think long-term, not short-term, but they too may want to give bonds a closer look.

Since most bonds have an inverse relationship with interest rates — that is, bond prices typically go down as interest rates go up — bonds are effectively on sale as interest rates rise. Because interest rates shot up from record lows in 2022, it was a historically bad year for bonds. However, as rates have stabilized, bonds are offering much higher rates than what investors could have received over the last decade, so investors should make sure they don’t neglect bonds in their asset allocations. Every investor’s situation is different, but bonds can make sense in many portfolios.

Investing in a higher interest rate environment is also a good time to remember that evaluating companies’ quality is critical to an investing plan. When interest rates were lower, many companies had more runway before turning a profit, since borrowing to fill the gaps was inexpensive. Similarly, early investors often had a lot of patience when it came to waiting on a company to fulfill its perceived potential, because the opportunity cost was relatively low while savings accounts and other relatively safe places to park cash paid little or nothing. Companies now may feel more financial pressure, implicit or explicit, to become profitable quickly while borrowing is more expensive or investors are less patient. As the market rallied in 2023, many investors increasingly came to value quality and stability over the potential for the next hot thing. Cryptocurrency and so-called meme stocks have largely fallen out of favor. Now investors are turning to companies with solid balance sheets and earnings potential.

Diversification is always important, but rising interest rates can be a useful reminder of this reality. Diversification protects against the risk that a single company, sector or region will have an outsize effect on your portfolio should something go wrong. I would not be surprised to see a variety of companies struggle or fail if they cannot refinance debt they took out when interest rates were extremely low.

Interest rates that are high — if not by historical standards, then at least in contrast to recent years — can require some adjustment. Whether you are borrowing, saving or investing, take the time to make sure your financial life is ready for the new reality we currently inhabit. And remember that rates can go up, or down, again. Stay flexible and respond to the circumstances in the present, not those you may have become comfortable with in the recent past.