The United States is invested in its taxpayers’ assets regardless of where those taxpayers live or where their assets reside. The complications of reporting foreign financial activities means that you can find out too late that you failed to tell the Internal Revenue Service something it needed to know.

There are a variety of circumstances that can lead to taxpayers needing to fix their foreign tax filings after the fact. First, it is worth noting that the requirements surrounding foreign accounts and holdings are complex, even by the arcane standards of the IRS. I will touch on these requirements in the next section, but many of them are relatively new and few are intuitive. A layperson without expert advice can easily miss one or more components of international tax filing requirements. So, too, can a person who is subject to the rules due to a one-time event, such as a large gift from a foreign individual or entity.

The second complication arises around taxpayers who are genuinely unaware that they need to deal with the American tax system at all. One category particularly prone to this are “accidental Americans”: people whose parents weren’t U.S. citizens but who happened to be present in the United States at the time of their child’s birth. U.S. citizens are subject to U.S. tax rules, regardless of where they reside. Former United Kingdom prime minister Boris Johnson provided a high-profile example when he renounced his U.S. citizenship in 2016 after receiving an unpleasant surprise in the form of an American tax bill on the sale of his London residence. (For more on accidental Americans, see my previous article “Tax Consequences Of Expatriation.”)

Similarly, noncitizens may qualify as residents for tax purposes if they visit the U.S. frequently enough. The substantial presence test applies to individuals who are physically present in the United States on at least 31 days in the current calendar year and a total of 183 days in the past three years. The IRS applies a formula that considers the proportion of the days an individual was present in the U.S. in each of the three years to determine if they meet the total days threshold. This test also applies to U.S. territories. If individuals trigger these rules, even if they principally reside in another country, they may be subject to IRS rules, including those pertaining to foreign accounts.

Foreign Filings: An Overview

The Hiring Incentives to Restore Employment Act became law in 2010. While it is not the only relevant piece of legislation when discussing Americans with foreign assets or accounts, it did create some major reporting requirements taxpayers should pay attention to when holding or managing assets overseas.

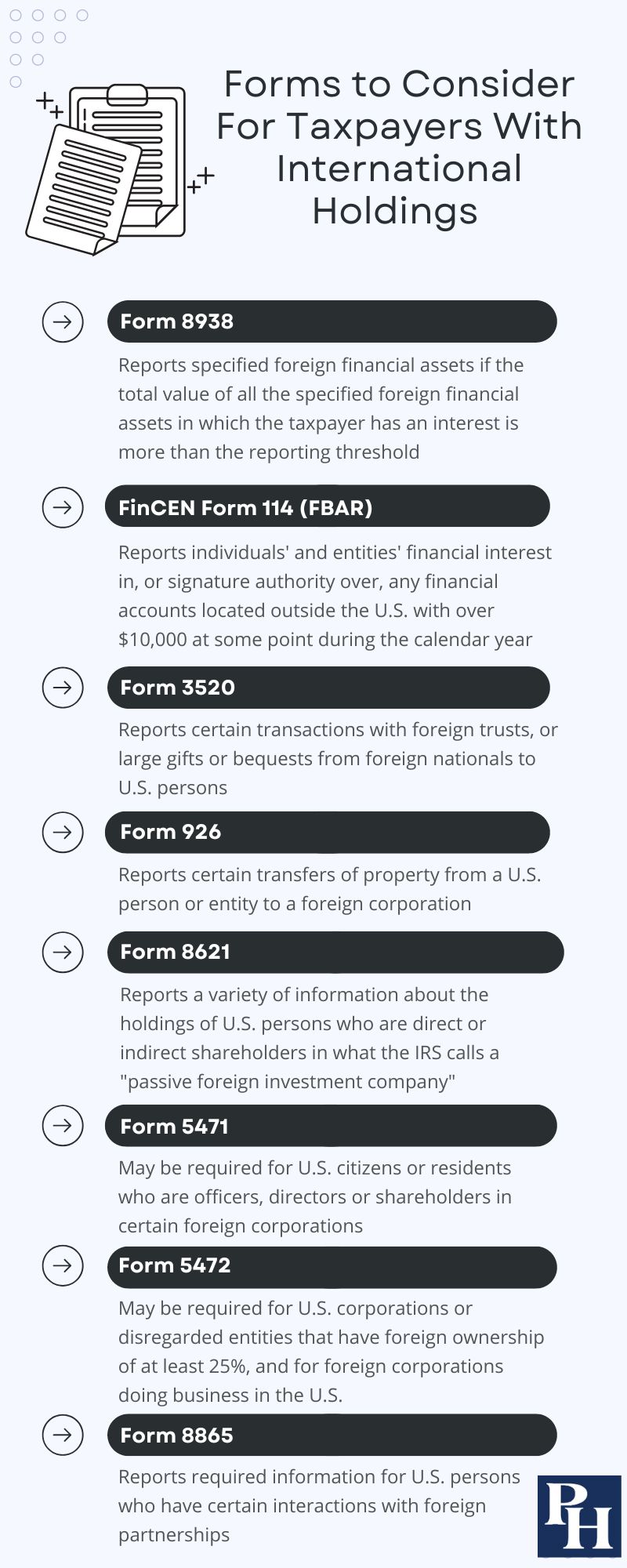

One component of the law was the Foreign Account Tax Compliance Act, or FATCA. Banks and financial institutions outside the United States that allow Americans to maintain accounts must generally report assets in those accounts. (This is largely why some financial institutions abroad do not allow U.S. taxpayers to open accounts at all.) The HIRE Act also mandated that certain U.S. taxpayers report their foreign assets on IRS Form 8938, either instead of or in addition to existing FinCEN Form 114 (previously Form TD F 90-22.1). I will discuss both of these in more detail below.

Lawmakers were concerned about American taxpayers keeping assets in offshore accounts specifically to avoid taxation. However, in light of the changed reporting requirements, taxpayers did have access to a voluntary disclosure program. This process wound down in 2018, so it is no longer an option for those with unreported foreign holdings.

Taxpayers who must file Form 8938 do so by attaching it to their annual income tax return. Taxpayers who don’t have to file a federal income tax return don’t have to file Form 8938, regardless of the amount of foreign assets they hold. Otherwise, unmarried individuals who reside in the U.S. and who had more than $50,000 in foreign assets on the last day of the tax year, or more than $75,000 at any point during the year, must file this form. For unmarried individuals residing outside the U.S., the thresholds are $200,000 and $300,000. The thresholds for married individuals are double the respective amounts for those residing inside and outside the United States. Failing to file Form 8938 can carry steep penalties: $10,000 plus underpayment penalties for any tax owed. If the taxpayer fails to file after an IRS notification, a penalty of up to $60,000 is possible, and criminal penalties may also apply.

FinCEN Form 114, commonly called the FBAR, is a separate document, not filed with an income tax return. U.S. taxpayers — both individuals and entities — must file an FBAR to report any financial interest in, or signature authority over, any financial accounts located outside the United States. For the filing requirement to kick in, the aggregate value of the taxpayer’s foreign accounts must exceed $10,000 at some point during the calendar year. The $10,000 threshold is calculated on a cumulative basis. For example, if an individual has three foreign accounts and the aggregate balance of the accounts exceeds $10,000 at any point during the year, all three accounts must be reported, even if no single account reached the $10,000 threshold. In addition, it does not matter whether the accounts produced any taxable income.

U.S. persons who must file an FBAR do so through a dedicated electronic system. (Paper filing is only allowed if the taxpayer requests an exemption from e-filing.) The form is due April 15, though an extension to October 15 is automatically allowed. Like Form 8938, the FBAR carries steep penalties for taxpayers who fail to file. However, in a taxpayer-friendly decision, the Supreme Court recently ruled that the $10,000 penalty for nonwillful failure to file applies on a per-form basis, rather than a per-account basis. The penalty for willful noncompliance is the greater of $100,000 or 50% of the account balances. For more on the similarities and differences between Form 8938 and the FBAR, consult this chart from the IRS.

In addition to these two main forms, some of the others that can affect taxpayers with specific international holdings or who are involved in certain international transactions are:

- Form 3520: Reports certain transactions with foreign trusts, or large gifts or bequests from foreign nationals to U.S. persons

- Form 926: Reports certain transfers of property from a U.S. person or entity to a foreign corporation

- Form 8621: Reports a variety of information about the holdings of U.S. persons who are direct or indirect shareholders in what the IRS calls a “passive foreign investment company” (for example, an offshore mutual fund)

- Form 5471: May be required for U.S. citizens or residents who are officers, directors or shareholders in certain foreign corporations

- Form 5472: May be required for U.S. corporations or disregarded entities that have foreign ownership of at least 25%, and for foreign corporations doing business in the U.S.

- Form 8865: Reports required information for U.S. persons who have certain interactions with foreign partnerships

Many taxpayers will rarely, if ever, encounter any of these situations, which increases the chances that individuals will fail to file the correct form or forms purely out of ignorance. While explaining every possible scenario is beyond this article’s scope, any financial interaction — whether business or personal — with a foreign individual, entity or financial institution makes it worthwhile to consult a tax professional with experience in international reporting requirements.

However, foresight is not always on a taxpayer’s side. What, then, should you do if you find out that you should have filed and failed to do so?

How To Fix Foreign Filing Failures

If you discover you should have been filing forms that you haven’t filed, the first thing to remember is the importance of being proactive. If the IRS discovers your mistake during an audit or investigation, your options narrow. The IRS tends to come down especially hard on foreign filing errors due to the presumption among legislators and government agents that unreported foreign accounts are a sign the taxpayer is trying to hide something. While acting before your hand is forced does not guarantee you won’t face penalties, your chances of a good outcome are much better if you come forward voluntarily.

For unintentional errors, the IRS does offer “streamlined compliance procedures.” If you failed to file a form detailing international accounts or transactions, these procedures offer the opportunity to come back into compliance with lower penalties, and under some circumstances, no penalties at all. Note that you must still pay any unpaid taxes that are due.

To qualify, the taxpayer must not have failed to file willfully. By the IRS’s definition, nonwillful behavior is “due to negligence, inadvertence, or mistake,” or behavior that is “the result of a good faith misunderstanding of the requirements of the law.” It is important to note that taxpayers cannot split up past actions; you cannot claim that some failures to file were nonwillful if other related failures were willful, as far as the IRS is concerned. However, taxpayers filing jointly may provide individual reasons for nonwillful actions. The IRS expects that taxpayers who use these procedures will comply with reporting requirements going forward, and taxpayers who use these procedures may be subject to a future exam.

Taxpayers using streamlined compliance procedures cannot be the subject of a civil examination or criminal investigation by the IRS for any year, regardless of whether the examination or investigation is related to the undisclosed foreign assets. Taxpayers also cannot have outstanding unpaid penalty assessments or exposure to significant civil penalties.

There are two sets of streamlined compliance procedures: foreign and domestic. For both processes, taxpayers must provide tax information for the three most recent tax years, including all required foreign information returns, and their six most recent FBARs. If the individual has come into compliance and reported international assets during this recent three-year period, but has missed reporting within the past six years, it can still make sense to take advantage of the compliance procedures to avoid potentially harsh penalties. For the same reason, taxpayers should retain records related to foreign accounts for at least six years, so they can be provided if the IRS requests them.

Streamlined Foreign Offshore Procedures

To use these procedures, taxpayers must meet the foreign residency requirement. For U.S. citizens and permanent residents, that means that in any one of the three most recent years, the taxpayer must not have had a “U.S. abode” and must have spent at least 330 days physically outside the United States. By the IRS definition, an abode is “where you maintain your family, economic, and personal ties.” Much like the concept of domicile, this definition can leave room for interpretation. If you plan to claim foreign residency and still own real estate in the United States, it may be helpful to consult a tax professional to ensure your case against a U.S. abode is well supported. Note that if you are married and filing jointly, both you and your spouse must pass the foreign residency test. For individuals who are not U.S. citizens or permanent residents, the requirement is that in any one of the three most recent years, the taxpayer cannot have met the substantial presence test.

A taxpayer who qualifies should start with Form 14653, in which he or she certifies that the failure to file previously was nonwillful. This form includes a narrative statement of facts, as well as a record of days outside the United States to confirm foreign residency. In addition, the filer should provide income tax returns (delinquent originals if they were never filed, or amended returns if they were filed without the relevant foreign reporting information). Note that Form 1040-NR is not accepted; the filer must provide Form 1040, Form 1040X or Form 1041. Along with these forms, the taxpayer should submit all tax that is due.

Properly submitted, the streamlined foreign offshore compliance procedures will impose no penalties. Note, however, that taxpayers will still be subject to any underpayment interest on unpaid taxes. The idea is to allow taxpayers outside the U.S. who genuinely did not know that they owed tax or that they were subject to reporting requirements to set things right with the American tax authorities by voluntarily coming forward.

Streamlined Domestic Offshore Procedures

Any taxpayers subject to U.S. tax and reporting requirements who do not meet the foreign residency test in the previous section should use the streamlined domestic offshore procedures instead. Unlike the foreign procedures, the domestic version is only available to those who have filed their required U.S. income tax returns for the most recent three years. This means that nonfilers with significant presence in the U.S. cannot use either set of procedures, and must come into compliance another way.

Taxpayers using the streamlined domestic offshore procedures follow a similar process to the streamlined foreign offshore procedures. They must also file a certification of nonwillful conduct — in this case, Form 14654 —including a narrative statement of facts, information about foreign financial assets, and the computation of a “miscellaneous offshore penalty.” They must also provide amended income tax returns; in contrast to the streamlined foreign offshore procedures, the domestic version does not allow taxpayers to provide delinquent income tax returns. Along with the forms, the taxpayer should submit all tax due as reflected in the amended returns (including underpayment interest).

The taxpayer owes the miscellaneous offshore penalty in lieu of, not in addition to, normal accuracy-related or FBAR penalties that would otherwise apply. This penalty is 5% of the highest aggregate year-end balance or value of the assets that are subject to the penalty during the covered tax return or FBAR period. This includes any asset that should have been reported on Form 8938 but was not; any asset that should have been reported on an FBAR but was not; or any asset which the taxpayer reported but for which he or she did not report gross income on their income tax return. The calculation is based on the highest year-end account balance and asset values among the years covered by the procedures.

FBAR Errors Only

In some cases, a taxpayer may have paid all necessary taxes on foreign assets but failed to properly file a required FBAR. If this failure was nonwillful, proactively filing delinquent FBARs can keep penalties to a minimum. If the Treasury Department finds that you had “reasonable cause” for your failure to file, you may not face any penalties at all. The IRS will not impose any failure to file penalties as long as you properly reported the income from the unreported foreign accounts and paid the associated tax, and you have not been previously contacted about delinquent returns for the years in question.

To file delinquent FBARs, you should submit the standard FBAR form electronically. On the cover page for the electronic filing, select a reason for filing late.

Delinquent International Information Returns

If taxpayers have reasonable cause for their failure to file international information returns, they may submit them late, as long as they are not under any ongoing civil examination or criminal investigation from the IRS. For most forms, the taxpayer will need to file an amended income tax return; Forms 3520 and 3520-A include separate instructions for filing. Taxpayers who are filing under the streamlined compliance procedures can submit delinquent information returns with those filings.

However you approach coming into compliance with the IRS (or, in the case of the FBAR, the Treasury Department), it is critical to follow all directions to the letter. Avoid rushing or taking any shortcuts. The penalties for delinquent or incorrectly filed forms regarding foreign assets and accounts are especially harsh, and if you hope to avoid or mitigate them, you will need to be sure you are putting yourself in the strongest possible position. You should also bear in mind that, in many cases, the failure to file an informational return or form means that your tax filings are incomplete in the eyes of the IRS, and so the statute of limitation for examination will not run until all required forms are filed.

As always when dealing with a complex tax situation, you should strongly consider letting a representative deal with the IRS on your behalf. A CPA, attorney or IRS-authorized enrolled agent will have the expert knowledge to keep the interaction professional and limited to the issues at hand.

Finally, regardless of how you approach the process, enter it knowing that you may need to be persistent. It may take quite some time, and many interactions with the tax authorities, to get everything straightened out. But while staying ahead of your reporting responsibilities in the first place is ideal, know that taking the time to proactively handle any problems offers the potential to save you considerable pain from harsh financial and legal penalties. It is also the right thing to do.