Navigating your Medicare options can feel complex. Deciding whether to enroll in original Medicare or a Medicare Advantage plan is often one of the most daunting choices among many, but understanding the pros and cons can help guide you.

While this choice applies to those first signing up for Medicare — in most cases, individuals a few months ahead of their 65th birthdays — it is not a one-time decision. Open enrollment season, which runs from Oct. 15 to Dec. 7, offers Medicare participants the opportunity to switch between a Medicare Advantage plan and original Medicare. This window is, in general, the only time participants can make such a switch (barring infrequent events that can trigger a special enrollment period).

Medicare Advantage plan participants can take advantage of a second window, from Jan. 1 to March 31. During this period, they can switch from one Medicare Advantage plan to another, or drop Medicare Advantage and opt for traditional Medicare. This is a one-way street, however; traditional Medicare participants can only switch to Medicare Advantage during the autumn open enrollment period.

Before jumping between plans, it is critical to understand how Medicare works and why your needs may change over time.

What Is Medicare Advantage?

As my colleague Larry Elkin explained in this space a few years ago, Medicare comes in four parts. Medicare Advantage plans are also known as Medicare Part C. They replace Parts A and B (which together are often called “original” or “traditional” Medicare). Depending on the plan, Medicare Advantage may also replace Part D, which covers prescription medication.

Medicare Advantage plans in more or less their current form began in the 1990s (though private plans have been part of Medicare in some capacity since the program’s inception in the 1960s). However, enrollment took off in the 2010s, after changes implemented by the Affordable Care Act. According to data from KFF, Medicare Advantage participation has risen from 25% of Medicare beneficiaries in 2010 to 54% in 2025.

Because Medicare Advantage plans are offered by private insurers, they are not a unified option like traditional Medicare. Instead, participants choose among plans available to them. Which plans are available depends on a variety of factors, including participants’ geographic location. KFF reported that the average individual had access to 42 Medicare Advantage options in 2025, and an average of 34 of those included prescription drug coverage.

The “pros” section to follow may suggest some of the reasons why Medicare Advantage participation has grown over the past 15 years. But the question is not whether Part C is a good idea in general. The question is whether a Medicare Advantage plan is right for you in particular.

Medicare Advantage Pros

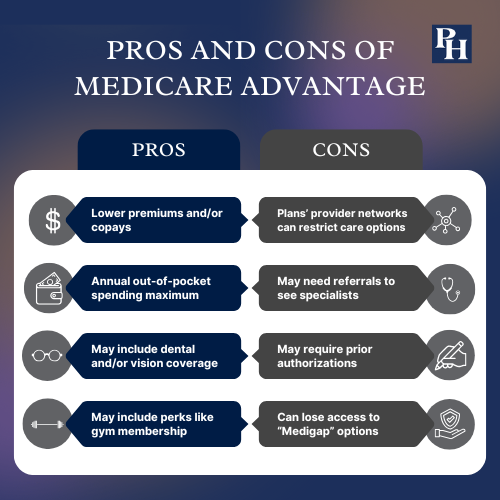

One of the major reasons that many participants favor Medicare Advantage is costs. While the details vary between plans, often the premiums are relatively low. Some plans go so far as to charge no additional premiums at all, beyond the required premium to match traditional Medicare. Additionally, cost-sharing may be less for many common services. Patients often pay set copay amounts such as $20 or $50 for a visit, as opposed to 20% coinsurance with traditional Medicare. If premiums are similar, it is easy to see how participants feel like they come out ahead.

Another cost factor is spending maximums. By law, Medicare Advantage plans must include an annual out-of-pocket maximum; some plans even undercut the required threshold. In contrast, original Medicare includes no cap on out-of-pocket spending. This difference can mean Medicare Advantage offers more peace of mind to some participants.

Beyond differences in price, Medicare Advantage plans typically boast expanded coverage compared to traditional Medicare. For example, plans may include dental or vision coverage, which Parts A and B do not include. Some plans include additional perks such as gym memberships or reimbursement for certain over-the-counter medications. Many providers tout their plans as a one-stop shop. Those who value a streamlined approach to their health care may find the centralized format of Medicare Advantage plans appealing.

Medicare Advantage Cons

While the type of care covered by Medicare Advantage plans may be expanded, the options for where beneficiaries can receive that care are restricted. Most Medicare Advantage plans come with their own networks of doctors, hospitals and other health care providers. Depending on the plan, participants may need a referral to see a specialist. And seeing providers outside the plan network may be more expensive, or not possible at all.

Provider networks are often restricted to a certain geographic area, too. For some participants, this may not be an issue. But for those with vacation homes, far-flung family, or lifestyles that keep them on the road, Medicare Advantage plans can cause more headaches than they cure. Even if you plan for routine and preventative care to take place near your primary home, a Medicare Advantage plan could restrict your options for emergency and urgent care while traveling. And individuals in rural communities may struggle to match available care with Medicare Advantage network options. By contrast, nearly every health care provider that takes any sort of insurance will accept traditional Medicare.

In addition to restrictions on providers, many Medicare Advantage plans require prior authorizations for certain procedures, office visits and medications. As anyone who has had to navigate this system knows, it can cause frustration and delay care. Note that while traditional Medicare currently does not require prior authorizations, this may be shifting. The Centers for Medicare and Medicaid Services announced a pilot program testing prior authorization requirements for certain services in six states starting in 2026. For now, however, prior authorizations are still mainly a Medicare Advantage concern.

As I mentioned earlier, you may switch from a Medicare Advantage plan to original Medicare during the open enrollment period. However, there is a major drawback to starting with Part C and then moving back to traditional Medicare: You may not have access to “Medigap” plans.

Medigap plans supplement traditional Medicare. You cannot purchase a Medigap plan while you participate in a Medicare Advantage plan. But buying a Medigap plan is often a one-time opportunity. If you don’t opt for traditional Medicare at the outset, insurers can take your age and any preexisting conditions into account if you later switch to traditional Medicare and shop for Medigap plans. At that point, you may find Medigap coverage prohibitively expensive or you may not be able to purchase it at all. Three states — Connecticut, Massachusetts and New York — are the exception to this rule, in that they require insurers to offer Medigap beyond the initial sign-up window. (Minnesota is set to join this list in 2026.) Unless you live in one of these states and plan to stay there, know that initially choosing Medicare Advantage may limit your options.

As you can see, personal factors including your travel habits, your financial situation, and your patience for restricted choices will contribute to deciding whether a Medicare Advantage plan is right for you. But as I suggested earlier, this decision is not something to “set and forget” from year to year.

The Future Of Medicare Advantage

While the “One Big Beautiful Bill Act” that became law in summer 2025 had a variety of impacts on Medicaid, the law made few major changes to Medicare directly. The biggest was that it restricts Medicare coverage to U.S. citizens, green-card holders, certain immigrants from Cuba and Haiti, and “COFA” immigrants from Pacific states with a special relationship to the United States. This eliminates formerly eligible individuals including refugees, asylum seekers, immigrants with temporary protected status, DACA beneficiaries (“Dreamers”) and others. Existing enrollees have a transition period until Jan. 4, 2027, but these rules apply immediately for new applicants.

The program may see an even broader impact from the OBBBA if, as expected, it significantly raises the national debt. Though the future of Medicare as a whole is beyond the scope of this article, it is not news to those who have followed discussions about the program that, absent major legislative changes, Medicare is likely to face significant funding challenges in the years to come.

It is worth noting, however, that Medicare Advantage programs may be changing sooner than the program as a whole. The reason is one that any American who needs health care can likely appreciate: Costs continue to rise. As the baby boomers transition from the so-called “young old” to the “old old,” Medicare Advantage plans may become a victim of their own success. They are apt to face a larger number of claims for more expensive services, with fewer new beneficiaries enrolling to offset the costs.

Some insurers have looked at raising out-of-pocket costs for beneficiaries, reducing coverage or both. Others have narrowed their Medicare Advantage plan offerings. UnitedHealthcare, the largest Medicare Advantage insurer, has said it will drop plans affecting 600,000 individuals in 2026. Even for those who don’t lose coverage outright, premiums and deductibles may rise.

Evaluating Your Medicare Advantage Options

If your insurer winds down your Medicare Advantage plan, the company may automatically enroll you in another of their offerings unless you opt out. Even if your plan is not going away, though, it is important to stay alert to changes. Your insurer will send you an “annual notice of change” (usually in September). It is important to read this document to understand any changes coming to your plan. In addition to costs, look for changes to your insurer’s network, and its formulary if it covers prescription drugs.

Your plan may also shift from one type of insurance to another. For example, preferred provider organizations, or PPOs, often allow you to see out-of-network providers for an additional fee. However, if your plan changes to become a health maintenance organization, or HMO, you may lose this option.

Whether you are evaluating changes to an existing plan or weighing your options as a new Medicare applicant, it is critical to consider more than just your monthly premiums. If you have doctors you like, find out whether they participate in the plan you are considering. If you already take maintenance medications, investigate how your plan’s formulary categorizes them (and note that this research may require phone calls or digging deeper than just reading plan documents). The Centers for Medicare and Medicaid Services rates Medicaid Advantage plans from 1 to 5 stars, which also can be useful supplementary information when evaluating your options.

All of this can be time-consuming, so if you are doing your own research, don’t procrastinate. You may find comparison tools from licensed health insurance marketplaces to be a useful way to get an apples-to-apples look at your options. Some publications offer their own online calculators. Government-run marketplaces, such as your state’s health insurance assistance program or the Medicare website, can help too.

Some people may find it helpful to turn to a professional. Reputable insurance brokers and financial planning professionals may be able to help with research and projections. Turning to a professional is not, however, a cure for procrastination. If you wait until November or early December, most professionals who handle Medicare Advantage evaluations will likely be swamped.

Medicare Advantage has its upsides, but whether it is right for you — and stays right for you — is a question you will have to answer for yourself. Like any insurance decision, due diligence, patience and proactive decision-making are key. Weigh the pros and cons carefully to find the right fit.

Editor’s Note: Beginning in January 2026, Sentinel articles will run first in our Substack newsletter. We hope you’ll join us as a subscriber. If you prefer to read articles on our website, they will become free to all 12 months after initial publication. Contact editorial manager Amy Laburda if you have any questions.