I know a lot of bright, well-read, capable people who were perplexed by the Medicare initial sign-up process, and who find the annual open enrollment period not much easier to navigate. Some of this, I found when I went through the process myself, was by design — and not necessarily the government’s design.

First, it’s important to understand that Medicare is an umbrella term for four different programs:

- Medicare Part A provides coverage for inpatient care at hospitals, as well as in certain other facilities such as skilled nursing facilities and hospice care providers.

- Medicare Part B covers health care expenses outside hospitals, including doctor visits, outpatient care, and preventative care like vaccines. It can also cover durable medical equipment including wheelchairs and walkers.

- Medicare Part C is a Medicare-approved plan offered by a private company. It serves in place of Parts A and B, and sometimes Part D as well.

- Medicare Part D helps to cover the costs of prescription medications.

We discuss the basics of these four options more thoroughly in our book Looking Ahead: Life, Family, Wealth and Business After 55.

Some of the confusion about Medicare centers on when to sign up, and on the financial penalties for not signing up when you first become eligible. This eligibility is still age 65 in the vast majority of cases, even though the normal retirement age for Social Security benefits is gradually rising to 67 for people born in 1960 or later. More specifically, the window for Medicare enrollment is usually three months before your 65th birthday to three months after, yielding a seven-month window. Millions of people become eligible for Medicare years before they actually retire. Others retire on Social Security (at reduced benefits) as early as age 62 but must wait until age 65 to get health insurance coverage under Medicare.

Starting later than age 65 can carry consequences. These vary by which part you delay. If you sign up for Part A later than you could have, your premium will rise by 10% (as long as you are not eligible for zero-premium Part A coverage, as I will discuss later in this article). You will pay this higher premium amount each month for twice the number of years you could have signed up but didn’t. For Part B, the penalty is 10% for every year you could have signed up but did not; you pay these higher rates indefinitely. And for Part D, the penalty is 1% for each month you could have signed up and didn’t — so 12% per year — and, like Part B, these higher rates persist as long as you participate. Note that there are some exceptions, such as qualifying for a special enrollment period for Part B, but be cautious all the same. (Note also that if you are already receiving Social Security benefits at age 65, you may be automatically enrolled in Medicare Parts A and B.) For the large majority of people, although not for everyone, the best time to sign up for Medicare is in the window that begins three months before turning age 65. This lets Medicare take effect as of the first day of the month in which the applicant’s 65th birthday occurs.

But what Medicare plan do you sign up for? Thanks to the ubiquity of modern databases and the marketing efficiency of health insurers, beneficiaries and beneficiaries-to-be find themselves inundated with advertisements for all-inclusive health plans that are pitched as “better” than Medicare. Many offer “zero premiums,” “zero deductible,” “zero co-pay,” “better-than-Medicare benefits” such as dental coverage, and even non-medical perks such as health club memberships. It sounds so good that there has to be a catch, right?

Right.

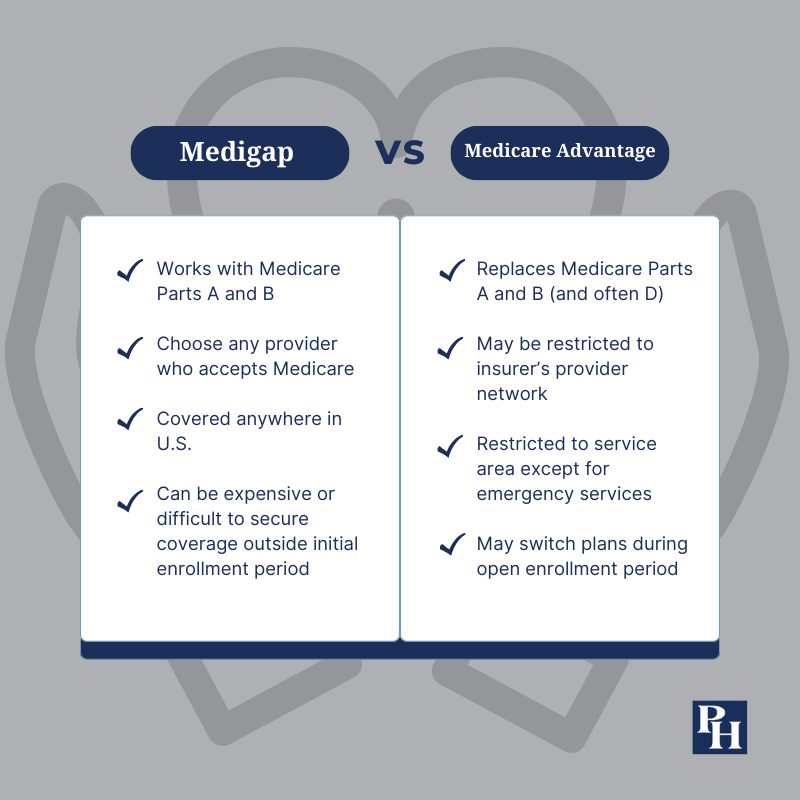

The major catch is that these plans each have their own network of doctors, hospitals, pharmacies and other service providers. Those networks are typically limited in geographic scope, and they may include a very limited number of specialists and advanced care facilities even within their home territory. This makes little difference for a healthy “young” retiree whose needs involve little more than an annual checkup and maybe a cholesterol-lowering daily statin pill. But some more elaborate forms of care may only be available in a limited number of places and after enduring a waiting list — if they are available at all. Medicare Advantage plans also often require prior authorization for many procedures and medications. And when retirees are on the road, these plans may only cover a limited amount of emergency care. The opportunity to change plans back to “traditional” Medicare generally comes along only once per year, in the annual enrollment period, unless you move out of your Medicare Advantage plan’s service area or qualify for a special enrollment period under some other limited exception.

Millions of people are happy to make these sacrifices in favor of the cost savings and expanded benefits that a Medicare Advantage plan offers. According to KFF, formerly the Kaiser Family Foundation, slightly more than half of Americans eligible for Medicare enrolled in such plans in 2023. I have no quarrel with their choice. That said, if you are a “snowbird” or otherwise split your time between disparate parts of the country; if you travel extensively; or if you prize the ability to choose from the widest set of providers without worrying about whether they are in-network, you probably won’t be among these satisfied customers. You’ll likely be much happier with some combination of Medicare Parts A, B and D, along with a Medigap plan.

It is important to understand the difference between Medicare Advantage plans and Medigap plans. Medigap coverage is not a substitute for Medicare Parts A, B and D, but rather a supplement to them. (At least to the first two; Medigap policies do not cover prescription drugs.) Participants buy Medigap coverage from a private insurer and use this coverage to help pay the patient’s share of costs in original Medicare. In most cases, you have six months to enroll in a Medigap plan, beginning in the first month where you both have Medicare Part B and are 65 or older. While it is possible to enroll in a Medigap plan after this window, you may have fewer options and they are likely to be more expensive. You cannot purchase a Medigap plan if you participate in a Medicare Advantage plan.

Medigap policies receive letter classifications, such as Plan G or Plan K, with benefits and limitations standardized between companies. The only difference among plans of a given letter grade is the premium cost, which can vary widely, and whether a particular insurer offers that plan in your ZIP code. A good place to start is with the AARP Medicare Supplement plan, which is underwritten by UnitedHealthcare. It requires AARP membership ($16 per year or less).

The nature of Medigap means that individuals can face a dilemma if they start on a Medicare Advantage plan and later want to switch to traditional Medicare. While this is possible, it usually means the beneficiary has missed the window in which insurers are obligated to sell Medigap policies regardless of any preexisting conditions or risk factors. While there are some other situations that can obligate insurers to offer coverage, and a few states require insurers to offer coverage at all times, many Medicare Advantage plan participants run the risk of being unable to secure supplemental coverage that is affordable, or being unable to secure such coverage at all.

For Medicare drug benefits (other than drugs administered during a hospital stay or certain outpatient procedures), you will need to sign up for Medicare Part D. KFF found that in 2023, beneficiaries could choose between an average of 24 Part D plans, with premiums ranging from $6 per month to $111 per month. Medicare.gov has a convenient and effective tool in which you can enter your current prescriptions and your ZIP code, and it will provide an estimate of your annual drug costs and premium payments for plans offered in your area.

Of course, you won’t know during your initial enrollment period, or the annual open enrollment periods that follow, whether your Part D plan is going to be the cheapest option if you get an expensive new prescription during the upcoming year, or whether it will stay the cheapest option in the following year even if your medications don’t change. Like most prescription drug plans, Part D plans include a formulary that divides medications into tiers, and those formularies differ between insurers. Adding complication, some plans designate certain pharmacies as “preferred,” so you could pay more at CVS than Walgreens, or vice versa. It’s worthwhile to check your situation each year during the annual enrollment period so you can change plans on Jan. 1 if doing so is to your advantage. Otherwise, you’ll be re-enrolled in your current plan by default.

If you want to make changes in your Medicare selections after the initial sign-up, you only have limited time windows (in most cases) to do it. The widest window is the annual Medicare open enrollment period, which runs from Oct. 15 to Dec. 7 for changes to take effect the following calendar year. During this window, you can freely change from traditional Medicare to Medicare Advantage plans or vice versa; add, drop or change a Part D prescription drug plan; or change from one Medicare Advantage plan to another. Once this window closes, you are locked into these decisions for most of the upcoming calendar year unless another exception applies. The biggest exception is the Medicare Advantage open enrollment period that runs from Jan. 1 to March 31. In this period, you can switch from one Medicare Advantage plan to another, or drop your Medicare Advantage plan and return to the traditional Medicare Part A, Part B and (if drug coverage is desired) Part D programs. But you can’t switch in the other direction, from traditional Medicare plans to Medicare Advantage, until the next autumn’s open enrollment period.

Medicare is essentially the biggest nationwide “network” of health providers on the market. If a provider accepts any insurance at all, traditional Medicare is likely first on the list, and it is often the least expensive option for its participants. A traditional Medicare plan, coupled with a Plan G supplement (the broadest coverage still sold in the Medigap market) and a Part D plan, is the most comprehensive coverage available to most of the general retiree market. Only some “Cadillac” government, union and corporate-executive plans without restricted provider networks compare.

Finally, how much does all this cost? As I’ve mentioned, some of it depends on which approach you take, as well as your location. But your income may also affect the answer. For most people, Part A premiums are based solely on how long the individual (or their spouse) worked. If you or your spouse worked for 40 calendar quarters — 10 years — or more in the U.S., you can expect no monthly premium. Part B, however, charges a monthly premium based on income. At this writing, individuals who earn $97,000 or less annually pay $164.90 per month for Part B. This also applies to married couples earning $194,000 or less. Above that threshold, premiums rise with income up to $500,000 (for individuals) or $750,000 (for couples). At or above that amount, monthly premiums are $560.50 in 2023. Part D premiums can also rise for higher-income beneficiaries.

Even with the maximum income-based surcharges, you’ll probably find that Medicare is a health insurance bargain compared to the premiums you or your employer would have paid on the private insurance market immediately before you signed up. Medicare is the country’s biggest single health care buyer, and it has the muscle to largely set its own pricing. Plus, it benefits from a dedicated revenue stream, in the form of payroll taxes, in addition to the premiums it charges. Yes, the Medicare program is built on financially shaky ground, but that’s a topic for another day. When you start enjoying all these Medicare benefits, remember to thank your working-age kids. They are doing a lot to help pay for it.