An executive sits on the board of a charitable organization. A successful alumna is a trustee of her alma mater. A young urbanite serves as a director of his condominium.

Many high achievers volunteer for such service as a way of giving back to their communities. These individuals often are called upon to chart an organization’s financial course, though only a few are trained as financial gurus. The rest usually get precious little guidance on how to develop a not-for-profit organization’s investment strategy.

Most organizations’ finances are similar to a household’s: There are routine inflows and outflows of cash, and there are windfall inflows and unanticipated expenses. Accumulated capital must be available to meet unexpected shortfalls, but if it is kept too liquid, a great deal of potential investment growth can be sacrificed. Good management is the art of anticipating cash flows and constructing a portfolio that keeps cash sufficiently available while supporting long-term growth.

Coordinating the money flows is referred to as asset and liability management (ALM). For example, a university endowment may begin its year with $50 million. During the course of the year, donors will make contributions, adding to the endowment’s assets. The endowment, often a separate entity from the university, will likely make distributions to the university during the year as well. Any specific commitments to distribute cash, such as a policy of distributing 5 percent of the endowment’s assets every year, are liabilities. The endowment’s portfolio managers should keep enough liquid assets on hand to at least cover any anticipated shortfall between current contributions and the endowment’s short-term liabilities. (“Liquid assets” refers to bank accounts and other short-term investments whose value does not fluctuate much, and from which cash can readily be withdrawn. Publicly traded stocks technically are liquid, since they are readily cashed in, but their value is too volatile to rely upon for short-term cash needs.)

Coordinating the money flows is referred to as asset and liability management (ALM). For example, a university endowment may begin its year with $50 million. During the course of the year, donors will make contributions, adding to the endowment’s assets. The endowment, often a separate entity from the university, will likely make distributions to the university during the year as well. Any specific commitments to distribute cash, such as a policy of distributing 5 percent of the endowment’s assets every year, are liabilities. The endowment’s portfolio managers should keep enough liquid assets on hand to at least cover any anticipated shortfall between current contributions and the endowment’s short-term liabilities. (“Liquid assets” refers to bank accounts and other short-term investments whose value does not fluctuate much, and from which cash can readily be withdrawn. Publicly traded stocks technically are liquid, since they are readily cashed in, but their value is too volatile to rely upon for short-term cash needs.)

A prudent investment plan for the portfolio should be based on a multiyear budget, i.e., five to 10 years. If a deficit is forecast in any of the first five years, the fund should invest the expected deficit amount in liquid assets such as bank CDs, money market funds and short-term bonds. This type of ALM schedule can be evaluated as often as necessary, though semiannually is sufficient for many organizations.

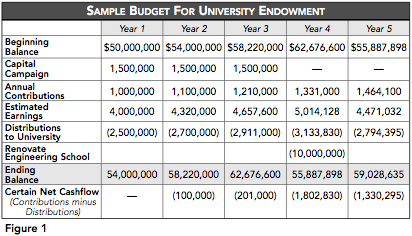

The example in Figure 1 outlines a multiyear budget for a well-established university endowment. It may reliably count on a certain level of annual contributions from donors. It also may count on pledges and other fund raising for a capital campaign to renovate the Engineering School in year four. That same endowment plans to make an annual distribution to the university’s operating fund equivalent to 5 percent of the previous year’s ending value.

In the short term, the stock market’s return from year to year can be quite volatile, but in the longer term, the return patterns tend to stabilize, which is how we arrive at the five-year rule of thumb. Based on data going back to 1926, there is a 90 percent chance that any dollar invested in the S&P 500 today will be worth at least one dollar five years hence. Unfortunately, achieving greater certainty requires much more time. To reach 95 percent confidence in one dollar invested today returning at least one dollar, one would need to commit eight years to the S&P 500. Diversified equity portfolios including small-cap and overseas stocks slightly increase the likelihood of a complete return of principal.

Once the current cash needs portion has been established, the board must decide on its risk tolerance. This decision is ultimately one of taste, but we tend to recommend that boards invest a good amount in equities for the long-term portion of their organization’s portfolio, especially after funds for all short-term needs have been set aside. The advantage of investing with a larger equity component is that the expected returns on the portfolio will rise. That may permit a college endowment to renovate an engineering building sooner; a pension plan to reduce its annual contribution, boosting the company’s bottom line; or a charity to expand its program services. Plus, stocks are the best way of beating inflation, a concern of many pensions.

If a deficit is forecast for years five through 10, the board can reasonably choose to invest these amounts in more aggressive holdings, though it should consider liquidity for years five through 10.

Figure 1 notes that “Certain Net Cashflow” (contributions less distributions excluding earnings) is negative in years two through five. The total aggregate certain net outflow for those years $3,434,125. This signals that the endowment should place at least $3,434,125 in non-volatile securities.

Any fund assets not expected to be withdrawn in the next five to 10 years should be invested in stocks and illiquid investments with equity-like returns, such as hedge funds, private equity funds and real estate.

Once a target asset allocation is set for an organization’s portfolio, the two vital elements are diversification and consistency. A portfolio that is not diversified may not perform as expected because company-specific risk factors can easily override asset-class considerations. Therefore, we strongly favor pooled investment vehicles, such as mutual funds and separately managed accounts, as the primary means of implementing the asset allocation strategy.

It is equally important to adhere to the asset allocation unless the organization’s financial objectives or situation materially change. There should be no attempt to time the markets. When rising markets lead to an over-concentration in one area, this is a signal to reduce the stake in that area. Conversely, when falling markets leave a segment underrepresented, this is a signal to increase investments in that segment. This is called “rebalancing the portfolio,” and it should be done at least annually, preferably quarterly.

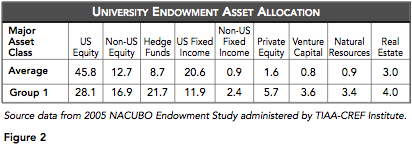

The 2005 National Association of College and University Business Officers Endowment Study by TIAA-CREF Institute demonstrates that the most successful endowments are those that recognize the need for significant equities and alternative investments. The study categorized 746 participating endowments into six groups by size. The largest category, Group 1, included endowments with more than $1 billion in assets. The smallest endowments, Group 6, had less than $25 million in assets.

Figure 2 compares asset allocations of Group 1 endowments to the average endowment (as determined by equally weighting the asset allocations of all participating endowments) as of June 2005.

Figure 2 compares asset allocations of Group 1 endowments to the average endowment (as determined by equally weighting the asset allocations of all participating endowments) as of June 2005.

The Group 1 endowments had less overall exposure to fixed-income and traditional equities and much larger allocations to alternative investments such as hedge funds, private equity, venture capital and natural resources.

The larger endowments performed better than the average endowment (as determined by equally weighting the returns of all participating endowments) in fiscal 2005. Since international stocks and bonds, real estate, private equity and natural resources had banner years in fiscal 2005, the larger institutions with greater allocations to alternative assets did better. But, even in less-than-stellar years, the larger institutions, again with higher allocations to nontraditional asset classes, performed better. For fiscal years 2000-2004, the larger endowments beat the average endowment in each individual year. The conclusions to draw from these data, both valid, are that the larger institutions have access to better money managers and their higher allocations to alternatives deliver superior returns.

Most hedge funds and private equity funds are exempt from Securities and Exchange Commission registration. To purchase these unregistered investments, a not-for-profit must meet certain asset thresholds, such as $5 million to be deemed an “accredited investor” and $25 million to be deemed a “qualified purchaser.” Therefore, some smaller endowments might not be permitted to participate in certain private investment funds. Further, in addition to investor qualification, some of the best private investment funds do not grant access to smaller players and those that have limited histories of private investing, though some investment advisers can help steer these smaller organizations into high-performing private investments.

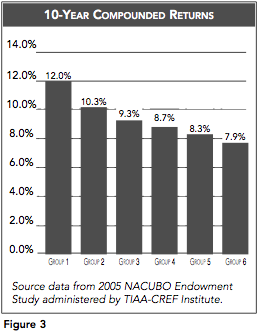

Predictably, the larger endowments, with access to better investments, have performed better over longer periods of time as well. The 10-year compounded returns for Group 1 for fiscal year-ended 2005 exceeded Group 2’s return. The 10-year compounded returns for Group 2 for fiscal year-ended 2005 exceeded Group 3’s return, and so on in a perfect linear pattern. See Figure 3.

Not-for-profits should exercise caution when making certain private investments because of Unrelated Business Taxable Income (UBTI). Most not-for-profits are exempt from income taxation on investment portfolio gains. However, when a hedge fund or private equity fund borrows to finance an investment, it may trigger UBTI, which would require the tax-exempt organization to pay income tax on the portion of income and gain derived from the indebtedness. Mindful of this tax, many private investment funds set up offshore mirrors of their domestic funds for not-for-profit investors. Income that would be subject to UBTI in a domestic fund will not be subject to UBTI if earned in an eligible offshore fund.

The fiduciaries of not-for-profit entities provide extraordinary, often unrecognized, value to their organizations. Unemotional, common-sense investing will further enhance their contributions.