Griping about free agency is a time-honored tradition among Major League Baseball fans. But for the past few years, it is players who seem to be finding free agency distasteful – or, at least, less appealing than the alternative.

Free agency is not entirely dead, as evidenced by Manny Machado’s $300 million, 10-year contract with the San Diego Padres. Machado briefly secured the largest free-agent deal in history, though he did not hold the distinction for long; shortly after, Bryce Harper chose to commit to the Philadelphia Phillies when the team offered a $330 million deal over 13 years. This deal made Harper the highest-paid team-sports athlete in history, outstripping not only Machado but also Giancarlo Stanton’s $325 million extension with the Miami Marlins in 2014, which Stanton signed prior to reaching free agency.

Ultimately, however, Machado and Harper are exceptions to the broader trend. Few teams these days regularly offer long-term, high-dollar-value contracts to players in their prime. Instead, an increasing number of young, up-and-coming players are forgoing the opportunity to become free agents in favor of signing multi-year contract extensions with their current teams. These extensions take players out of free agency market until they are past, and sometimes well past, age 30. And while contract extensions can sometimes be lucrative in their own right – Los Angeles Angels center fielder Mike Trout recently displaced Harper’s record with an extension worth approximately $430 million over 12 years – usually an extension means forgoing the potential of a larger deal in favor of security.

Why are players increasingly making this trade-off?

Part of players’ caution comes from the overall state of the league. As The Wall Street Journal noted in February, labor relations between teams and players are tense right now, with fears of a work stoppage after the 2021 season looming large. In this atmosphere, free agency is beginning to look deeply risky. After all, it took months for Machado and Harper to secure their respective deals, while NBA teams are still snapping up high-profile free agents within days of their entry into the market. As of March 1 – less than a full month before the season began – more than 70 major league players still had no contract. Essentially, younger players who take contract extensions are giving team owners potential discounts on their future performance in exchange for an upfront commitment.

Commitment can weigh even with free agents these days. ESPN reported that Harper may have had larger offers from other teams but was convinced by the Phillies’ long-term commitment. His 13-year contract tied the record for length, and came with no opt-outs and a no-trade clause, which will mean Harper may well play in Philadelphia for the rest of his career. If Harper had preferred a short-term contract and a second chance at free agency, he surely could have chosen that alternative. Instead, he told his agent that he wanted a lifetime deal, even at the cost of a lower annual salary.

For more evidence that players are becoming more cautious in general, consider Jacob deGrom’s negotiations with the New York Mets. The team and deGrom announced in advance that they would cease potential contract extension talks on opening day if they couldn’t reach an agreement by then. Negotiations went down to the wire, but on March 26, two days before the deadline, the team confirmed that deGrom had agreed to a five-year contract extension. Had they not reached an agreement, deGrom reportedly had planned to limit his workload in order to lower the risk of potential injury ahead of achieving free agency following the 2020 season.

In this environment, it may not be clear to a given player how best to proceed. Say a player is in his mid-20s and is an established star, a few seasons away from eligibility for free agency – that is, six years of major-league play. If he locks himself into a relatively small deal, the money is guaranteed, no matter what happens in his career. If he turns the extension down and waits for free agency, he could secure a significantly more lucrative contract – assuming a team is willing to offer one. But waiting also represents risk in the form of potential injury or other changes for the worse in a player’s performance.

As is the case for many financial planning questions, there is no one right answer to whether a player should secure an extension at a relatively lower dollar amount or sacrifice some security in search of a larger payday. In essence, a player asking this question is asking whether the offer from their current team is “enough.” Is a shot at a bigger payout worth the risk of forgoing a sure thing? One way to find an answer is to perform – or have a professional perform – a risk-reward analysis.

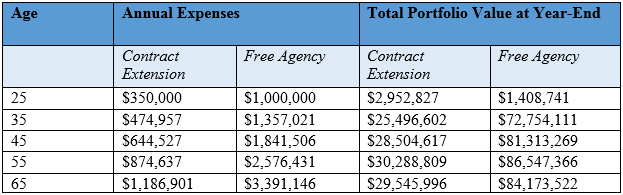

We used Yankees pitcher Luis Severino as a test case. Severino, who is 24 years old, recently signed a four-year deal, with a fifth-year option, worth up to $52.25 million assuming the Yankees keep him on for the fifth year. We ran two projections of his potential cash flow: one with his contract extension, and another where he held out and signed a major free agency deal a few years down the line. We roughly tripled his payday to $150 million, paid over six years, in this hypothetical version of events.

In both projections, we assumed Severino would buy a house worth about 10 percent of his overall contract: $5 million in version A and $15 million in version B. In the first scenario, we assume Severino will retire at age 30, while in the second we assume he will retire at age 34 to account for the later start of the free agency contract. In neither case did we assume he would have a second-act career, though many former players do go on to work as broadcasters, entrepreneurs and authors, among other professions. We assumed 3.1 percent inflation, a long-term average based on historical data, and a 6 percent return on an investment portfolio, which represents a relatively conservative investment approach. We set annual tax at 45.82 percent, though the specific rate would actually vary based on the state and local taxes due, as well as any changes to the federal tax regime.

As all of these assumptions suggest, a risk-reward analysis is inherently based on estimates. But the results are still useful when approaching the problem.

In this projection, we started from the total potential contract value Severino could expect in each scenario, and then worked back to determine his baseline annual spending, assuming he lives to be 90 years old. The question we were attempting to answer was, essentially, would both contracts give Severino “enough” to live on comfortably without other sources of income, assuming he invests prudently to keep ahead of inflation.

In scenario A, based on Severino’s actual contract extension, $52.25 million becomes about $23 million after taxes. If he prudently invests this amount, Severino can expect to see an additional $64 million over the course of his life. This equates to annual spending of about $350,000 in the first year, rising by inflation to $1.2 million a year in spending by age 65. Assuming he is able to make and stick to a reasonable financial plan, Severino should never need to work again unless he wishes to. Yes, he would certainly have even more money if he secured the free agency contract – but he would risk an outcome where he gets much less if, for instance, he suffers a career-ending injury before he can enter the free-agent market. And, while we didn’t allow for this possibility in our examples, it is worth noting that Severino may still enter the free-agent market at age 29, potentially increasing his total career earnings yet again. If Severino does take the risk and hold out for the big free-agent contract, his annual spending could be $1 million in the first year, rising to $3.4 million per year at age 65, as shown in scenario B.

Of course, no plan remains pristine and unchanged over the entire course of a person’s life. In reality, you would never make a financial plan at age 25 and leave it untouched for decades. Most players’ spending will be front-loaded, as they acquire houses and raise their families during and immediately following their MLB careers, which can affect how these estimates play out. When running projections, it is also important bear in mind that each year’s spending won’t be the same, even aside from inflation, as children grow up and eventually move out. Instead of serving as a crystal ball, this sort of analysis allows you to see a reasonable approximation as to how your money relates to your desired lifestyle once you are long past the end of your career.

That desired lifestyle directly contributes to answering the question of whether a given contract amount is enough, whether a player is evaluating a given offer or deciding how much to ask for in negotiations. A particular player will need to consider some fundamental questions when setting up this sort of projection, the first and most important of which is: Where do you want to live? Different parts of the country have different costs of living, and especially impose widely different levels of tax, which can mean a dollar goes further in less expensive parts of the country. As an example, a report from NBC suggested California’s hefty state tax burden and higher cost of living may have handicapped multiple teams, especially the San Francisco Giants, in the bidding war for Harper.

Any amount beyond this baseline is “extra” as far as financial planning is concerned. You can use it to inflate your lifestyle, support charitable causes, increase the amount you plan to pass to your heirs or pursue other financial goals. Having more cash to throw at these goals is nice, but when you are choosing between securing a sure thing and taking a risk, it’s important to understand what is or is not extraneous to your fundamental goals.

The risk-reward calculation may also look different from an agent’s point of view. If an agent relies principally or entirely on one client, he or she may not want to take on the risk of holding out for free agency, even if the potential payout is much larger. On the other hand, agents who work with many players have diversified away some of their risk, so they may encourage a player to take the risk of waiting, especially if they worry that players deferring free agency may broadly depress the market.

Ultimately, the decision to settle for a smaller payday in order to secure peace of mind is one every individual player will have to make for himself. But a thoughtful, methodical approach shows that there is no need to make such a decision entirely in the dark when it comes to the potential financial consequences.

{kind=link}