Many Americans only think about their taxes for a few weeks of the year: from when they get their W‑2 until they file their income tax return.

These taxpayers may be surprised that some people are currently in the thick of tax season. For some, autumn not only brings back-to-school shopping and colorful leaves, but also a final review of their annual income tax return.

As a tax professional, I will note that optimal tax planning is a year-round process, regardless of your financial situation. Freelancers and sole proprietors need to handle estimated income taxes quarterly, for example. Even taxpayers with relatively straightforward financial situations can benefit from incorporating tax planning into their overall approach to spending, saving and investing. That said, there is a particular “echo” of spring tax season in the fall. This is because a typical request of a six-month extension to file a federal tax return generally gives taxpayers a due date in mid-October.

The Internal Revenue Service allows taxpayers to file Form 4868 to request such an extension. As long as you file the extension by the original return’s due date, the IRS grants such requests automatically. Note, however, that this is an extension to file, not to pay: You must pay all taxes due by the original filing deadline.

Even if the tax authorities don’t demand a reason for an extension, taxpayers who have never needed one may wonder why such a form is necessary. There are a variety of reasons a taxpayer could need an extension, many well beyond the scope of this article. But a frequent one is waiting on a form that an organization has not yet issued to you. Some of the most common forms that leave taxpayers waiting are Schedule K-1 and, more recently, Schedules K-2 and K-3. If you are new to these forms, I will break each of them down briefly.

What Does A Schedule K-1 Include And Who Gets It?

A “schedule” is an additional form the IRS requires for a taxpayer to provide more information about certain kinds of deductions or income. A Schedule K-1 (often just shortened to “K-1”) is a tax form that taxpayers usually receive, rather than one that they must fill out themselves.

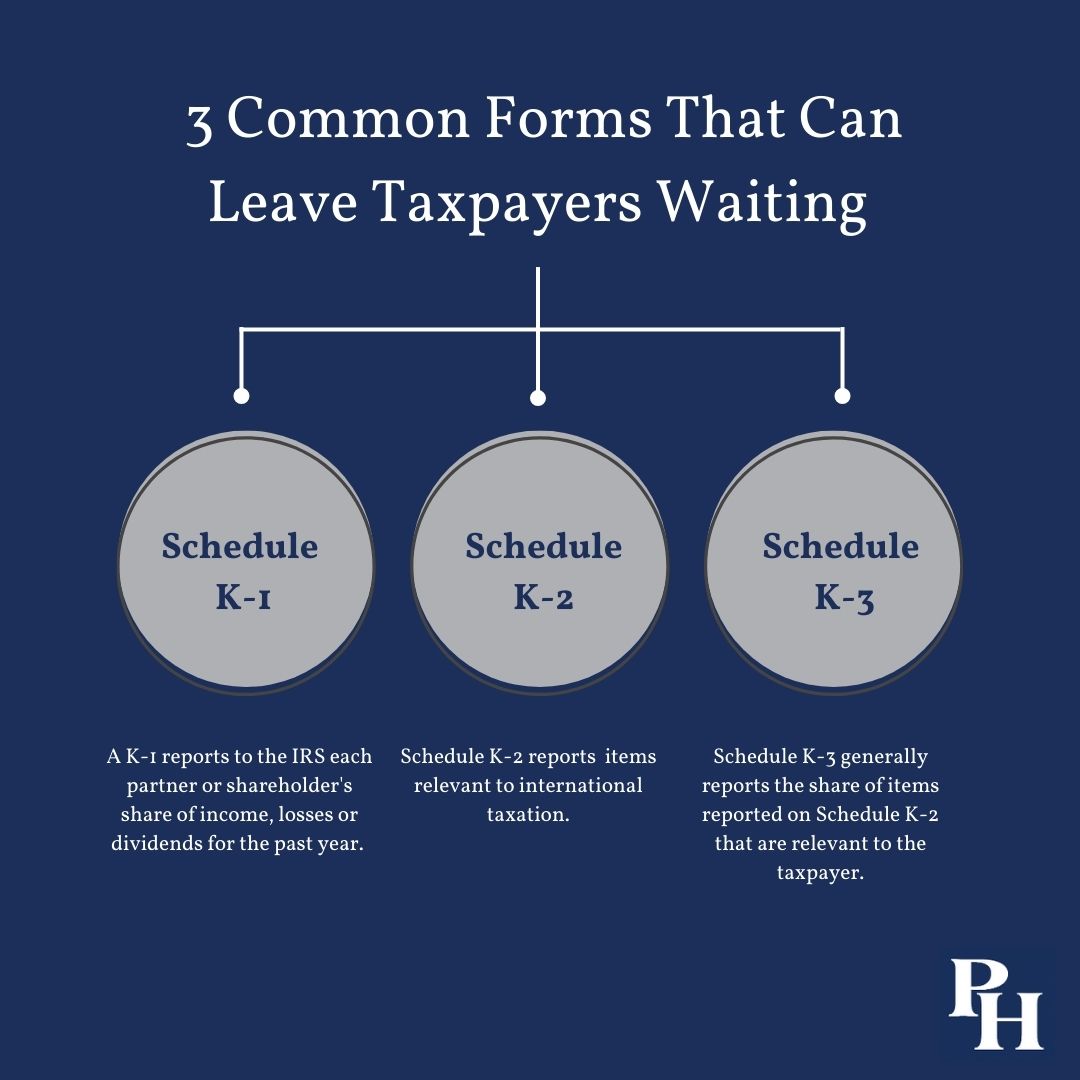

Certain “pass-through” entities, such as partnerships, limited liability companies and S corporations, issue K-1s to partners or shareholders each year. These organizations are called pass-through businesses because earnings “pass” to the partners or shareholders for tax purposes. This means earnings are taxed at the individual rate rather than the corporate tax rate that applies to businesses like C corporations. A K-1 reports to the IRS each partner or shareholder’s share of income, losses or dividends for the past year.

A Schedule K-1 is the result of different IRS forms depending on the organization that issues it. Partnerships file Form 1065, while S corporations file Form 1120-S. Individuals may also receive a K-1 if they are the beneficiary of a trust or an estate. The details can vary, and it is wise to involve a tax professional if you receive K-1s from any source. But broadly, all of these situations involve reporting income or losses. As such, they can either increase a recipient’s tax liability or they can provide potential income tax deductions.

Receiving one or more K-1s does not always mean you need to file for an extension. In general, entities must issue K-1s by March 15, leaving partners or shareholders sufficient time to prepare an individual return. However, as with individuals, entities can request six-month extensions of time to file their tax returns, in which case a partner might not receive their K-1 until Sept. 15. Also, K-1s can introduce special complexity, because the forms may come with additional information such as disclosures, raw data and supplementary statements. Dealing with K-1s can be a labor-intensive exercise, so taxpayers with multiple K-1s may want to take advantage of an extension just to deal with these additional complexities.

What About Schedules K-2 And K-3?

Schedules K-2 and K-3 are relatively new; the IRS only started requiring them beginning with the 2021 tax year. Both have to do with international taxes, an area that is notoriously complex. The new forms are intended to make reporting more straightforward. The format for these new forms is standardized. The new forms also reflect rules introduced in 2017’s Tax Cuts and Jobs Act that affect the calculation of international tax liabilities.

Pass-through entities with items of “international tax relevance” must issue the new forms. Individual taxpayers who must file Form 8865 (“Return of U.S. Persons With Respect to Certain Foreign Partnerships”) must fill out these schedules as well. This raises the question of what the IRS considers “items of international tax relevance.” As with many tax questions, the answer is not cut-and-dried. But guidance thus far has suggested that tax authorities will take a wide view. In addition to foreign-source income and offshore assets, entities that claim a foreign tax credit or that have interests in foreign-controlled corporations may also need to file.

Schedule K-2 reports any items relevant to international taxation that arise from a partnership. Schedule K-3 generally reports the share of items reported on Schedule K-2 that are relevant to the taxpayer. These forms apply to entities or individuals filing Form 1065, Form 1120-S or Form 8865. Certain domestic partnerships are exempt from filing, but the rules are complex enough that they are beyond the scope of this article; partners should consult a tax professional with experience in international taxation to parse them.

In fact, individuals who receive a K-2 or K-3 should take it as a good indication that they should consider other possible foreign tax reporting requirements. As my colleagues and I have written often in this space, foreign tax obligations can be especially complicated. Prudent taxpayers — whether partners, shareholders or other stakeholders — should involve an experienced professional and avoid trying to DIY a tax situation that includes exposure to foreign income or assets.

Schedules K-2 and K-3, as part of Form 1065, must be issued by March 15 unless the partnership files for an extension. As with K-1s, and arguably more so, taxpayers who receive these forms should try to ensure that they and the professionals they employ have plenty of time to review and process these forms before they file their income tax returns.

An Autumn Data Dump

It is wise to keep track of which K-1s (and, now, K-2s and K-3s) you expect to receive. While entities have the responsibility to issue these forms, as a taxpayer, you must also stay alert for any forms that might have gone astray, been overlooked or otherwise slipped between the cracks. As a first step, check which forms you received last year as a baseline, and consider keeping a central list of those you have received for the current tax year.

More broadly, keeping accurate records throughout the year will save you from a last-minute scramble, whether in the spring or the fall. You should create a system that works for you, whether digital, physical or a combination of the two. It is also a good idea to keep your tax preparer apprised throughout the year of the forms you receive, in whatever way he or she prefers. Knowing what to expect can keep you calm ahead of IRS deadlines. It can also give your tax preparer the opportunity to adequately advise you on how to best handle your return.

Ideally, a well-organized system will also provide for keeping records of previously filed returns organized and accessible. These records are important not only in case of a potential audit, but also for your own reference in situations where you may have to estimate future income or check that you have received all the tax data that you expected.

Schedules K-1, K-2 and K-3 are among the many reasons you may handle your taxes in the fall rather than in the spring. But regardless of when you file your return, keeping an eye out for tax data all year long is the prudent thing to do.