One year ago on this page, I questioned whether any lessons had been learned from the decade-long housing bubble.

The U.S. taxpayer has since been put on the hook for hundreds of billions of dollars of losses that should have been borne by private parties. But apart from this, the change resulting from this debacle has been disturbingly slight.

The Federal Reserve and the Treasury have concentrated on keeping the global financial system afloat. Last month’s failure of Lehman Brothers demonstrated how one institution’s default can freeze credit markets and create a chain reaction. In this case, one large money market mutual fund “broke the buck,” causing investors to lose an estimated 3 percent of the cash they parked there, and several funds had to delay redemptions.

Nothing has been done to fix the problems in the mortgage industry that led to this mess. Once conditions stabilize, lenders still would have incentives to issue loans freely, sell them off to investors, pocket the origination fees and find new borrowers. Investors or taxpayers are left holding the bag when loans cannot be repaid. Once the housing market recovers and the immediate credit shortage eases, the same problems can happen again.

Some practical changes that could be made, but have not been, include:

- Prohibiting consumer mortgages that include up-front points, prepayment penalties and “negative amortization” features that allow the loan balance to rise even though the value of the property may be stagnant or falling. Points and prepayment penalties usually are bad deals because people move or refinance before a mortgage is paid. Unsophisticated borrowers do not readily understand these costs. Negative amortization creates a trap that can lock a homeowner in place or force a default. Loans should be realistically priced through the interest rate. If the borrower cannot pay, don’t make the loan.

- Preventing originating lenders from transferring the entire loan within the first five years, or require proceeds from loan sales to be escrowed and released only gradually. The lender is much better able to evaluate the borrower’s condition than is a subsequent investor, but there is no incentive for the lender to care unless he remains at risk. This rule will slow the pace of lending, but the quality of consumer loans would be higher.

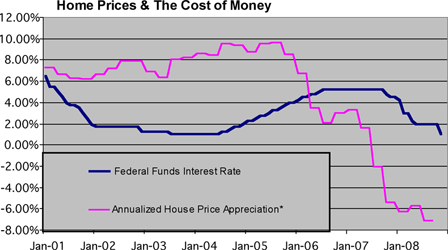

- Getting rid of the tax subsidy for mortgage interest, or at least for home equity lines and other second mortgages. Until 1986, all U.S. consumer interest was tax-deductible. That year’s tax law created an advantage for mortgages and home equity lines that was irresistible to consumers, even though advisers always warned that people would end up losing their homes if they could not repay. Today, that warning has come true. Artificially cheap mortgage money also creates overinvestment in housing. The National Association of Home Builders reports that the average new house swelled from 1,725 square feet in 1985 to 2,469 square feet in 2006. This is a significant speed-up in the growth rate. The average new home in 1970 was 1,500 square feet.

- Requiring banks to release their liens on properties whose home equity lines have been frozen. Hundreds of thousands of Americans have had their credit lines turned off because the issuing banks, realizing that home values have fallen, refuse to allow consumers to draw on previously authorized lines. This is reasonable, since banks should not make mortgage loans without property values to back them up. But banks should be required to release their claims on such property for the undrawn amount of the credit line. This would free consumers to find other lenders.

In just over a year, the housing-driven credit squeeze took out Bear Stearns, Fannie Mae, Freddie Mac, Lehman Brothers and about a dozen banks and mortgage companies, including Washington Mutual, the biggest bank failure in U.S. history. Washington was forced to effectively nationalize American International Group, the country’s biggest insurer. American taxpayers are being asked to mop up the mess, just as they did when the savings and loan industry crashed 20 years ago.

The problems that brought down the S&Ls have now repeated themselves. This time, maybe we can learn from our mistakes.